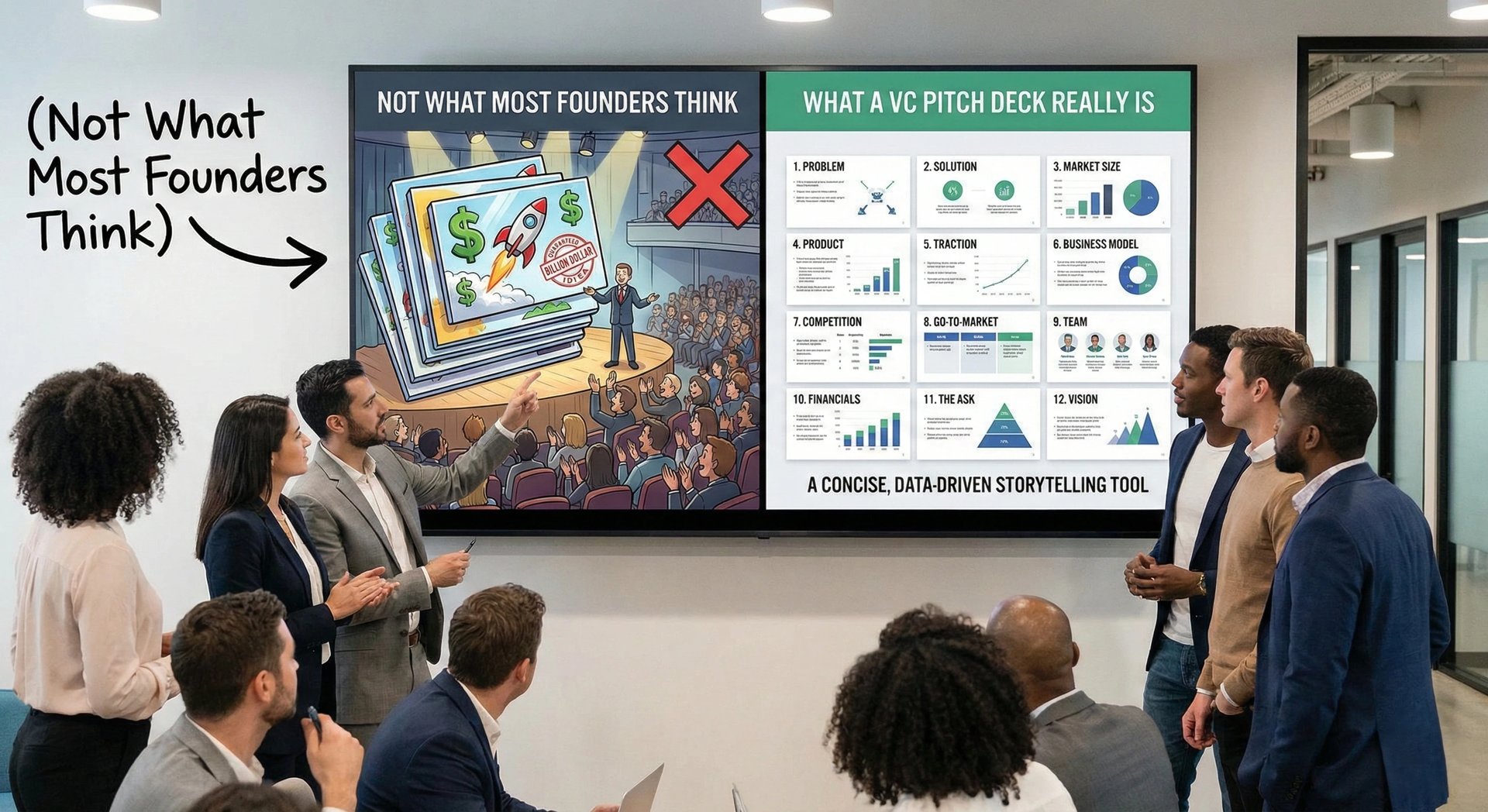

What a VC Pitch Deck Really Is (Not What Most Founders Think)

A VC Pitch Deck is not a marketing brochure; it is a "Financial Option Contract." The forensic definition that separates investable assets from noise in 2026.

1.1: WHAT A VC PITCH DECK ACTUALLY IS?

1/14/20265 min read

If you are a Seed or Series A founder building a deck in 2026, you are likely operating under a fatal misconception.

You believe your pitch deck is a marketing document designed to sell a product. You are wrong. A pitch deck is a securitized asset prospectus. It is a financial instrument designed to sell equity, not software.

When you treat your deck as a narrative about "user delight" rather than a logic gate for capital allocation, you are not just failing to raise; you are signaling to me—the analyst holding the checkbook—that you do not understand the asset class you are trying to enter. In the current high-interest rate environment, capital is not "fuel for dreams"; it is expensive leverage. To understand why 99% of decks fail the initial screening, you must first understand What a VC Pitch Deck Actually Is (and What Investors Mean When They Ask for One). This is not a nuance. It is the foundational layer between a "pass" and a Partner Meeting.

The Forensic Diagnosis

Why does the "Product-First" error destroy fundraises with such high lethality? Because it forces a Venture Capitalist to do the work you should have done for them.

The "Red Flag" Scenario

I see this approximately 15 times a day. A founder sends a 20-slide deck. Slides 4 through 12 are high-fidelity screenshots of the UI, detailed explanations of the "proprietary algorithm," and quotes from happy beta testers.

What you see: A demonstration of product excellence and market fit.

What I see: A hobbyist. A Product Manager masquerading as a CEO.

When a deck focuses on the what (the product) rather than the how (the business model and capital efficiency), the investor’s internal monologue shifts immediately from "How big can this get?" to "How much will this burn?"

Psychological Audit: The Builder's Bias

This error stems from "Builder’s Bias." You have spent 18 months agonizing over code, design, and user flows. Your ego is tied to the product’s function. Therefore, you assume the investor’s primary risk is technical (Does it work?).

In reality, for 90% of B2B SaaS and consumer apps, the technical risk is zero. We know you can build it. The risk is distribution and unit economics. By focusing on the product, you are solving for a variable I solved for in the first 30 seconds. You are ignoring the actual variables that determine fund returns: CAC, LTV, and market depth. You are answering a question nobody asked.

The Mathematical Proof / The "Why"

Let’s strip away the sentiment and look at the math of the Venture Capital funnel. An associate at a Tier-1 firm reviews roughly 2,000 decks a year to make 2–4 investments.

The Cognitive Load Equation:

Time Per Deck = 140 seconds

If your deck requires me to interpret your business model, you have introduced "Cognitive Friction." Every second I spend trying to figure out how you make money is a second I am not spending calculating the potential return.

The Cost of Ambiguity

In probability theory, VCs are trying to minimize Type I errors (investing in a dud) and Type II errors (missing a unicorn). However, the cost of a false positive (a bad investment) is visible and painful—it ruins the fund's IRR (Internal Rate of Return).

Therefore, the default state of a VC is "No." We are looking for reasons to reject, not reasons to accept.

Metric Ambiguity: If you show "User Growth" instead of "Revenue Growth," I assume you have no revenue.

TAM Inflation: If you claim a $50B TAM without a bottom-up calculation, I assume you are lazy.

Design Clutter: If a slide has more than one core thesis, I assume your strategic thinking is equally cluttered.

The Dilution Logic

Founders often fail to demonstrate how the capital injection converts to enterprise value.

If you are raising $5M at a $20M pre-money valuation (20% dilution), you need to prove that this $5M will effectively triple the valuation to $60M+ before the next round. If your deck focuses on product features, you have provided zero mathematical evidence that you can execute that 3x multiplier. You have shown me a toy, not a lever for asset appreciation.

The "Insider" Solution Protocol

To fix this, you must pivot your deck from a "Product Tour" to a "Capital Allocation Thesis." This requires a forensic overhaul of your narrative architecture.

The Before vs. After

The Weak Version (Product Focus):

Slide Header: "Our Solution: An AI-Powered Workflow Tool."

Content: Screenshots of the dashboard, list of features, tech stack details.

Result: Investor asks about technical feasibility (low value).

The VC-Ready Version (Asset Focus):

Slide Header: "Unlocking 80% Gross Margins via Automated Workflows."

Content: Flowchart showing how the AI replaces manual labor costs, creating a permanent arbitrage in the customer's P&L.

Result: Investor asks about pricing power and retention (high value).

The "De-Risking Velocity" Framework

Your deck must prove that every dollar invested reduces a specific risk. Structure your narrative using this logic:

The Arbitrage (Problem/Solution): Do not just state the problem. Quantify the inefficiency in the market. "Companies spend $10B annually on process X. Our protocol reduces this to $2B, capturing $1B in value."

The Engine (Business Model): How do you extract value? Recurring revenue? Transaction fees?

The Fuel Efficiency (Traction/Metrics):

Use the Burn Multiple logic.

Burn Multiple = Net Burn

Net New ARR

If your Burn Multiple is under 1.5x, highlight it. It proves you are a disciplined capital allocator. If you don't show this, I assume your Burn Multiple is 3x or higher.

The Terminal Value (The Ask):

Do not ask for "18 months of runway." Ask for "The resources required to achieve $2M ARR and unlock Series B." Frame the cash as a bridge to a specific valuation milestone, not a safety net for salary.

The "Death Traps"

As you attempt to professionalize your deck, avoid these common over-corrections that I see savvy founders make:

The "Investment Banker" Slide:

Do not fill a slide with a dense Excel grid of 5-year financial projections. Nobody believes you know what your revenue will be in 2030. Limit projections to 18-24 months (the runway of the round) and keep them grounded in logic, not fantasy.

The "Logo Salad" without Context:

Putting 20 logos of "partners" or "customers" on a slide is meaningless if they are pilots or LOIs (Letters of Intent). Be precise. Label them: "Active Contracts," "Paid Pilots," or "LOIs." Ambiguity here looks like fraud during due diligence.

The "2021 Valuation" Trap:

Do not use valuation multiples from the zero-interest rate era (ZIRP) to justify your current ask. If you reference a competitor who raised at 100x ARR in 2021, you look out of touch. Benchmark against current public market multiples (roughly 6x-12x ARR for high-growth SaaS).

The "High-Ticket" Conclusion

The difference between a deck that gets read and a deck that gets funded is not the quality of the graphic design; it is the quality of the financial logic. By restructuring your deck as an asset prospectus, you shift the VC's perception of you from "enthusiastic inventor" to "disciplined CEO." In a tight market, this perception shift alone is worth $1M+ in pre-money valuation. For a comprehensive breakdown of the entire ecosystem, read How VC Pitch Decks Really Work in 2026 (Not What Founders Think).

The Filter:

You can spend months A/B testing your slides against rejection emails, or you can use the Slide-By-Slide VC Instruction Guide included in our $5k Consultant Replacement Kit. It contains the exact logic flow, header structures, and metric requirements that Series A auditors look for. Price: $497. Available on the home page. If you are serious about treating your startup as a financial asset, this is your toolkit.

Funding Blueprint

© 2026 Funding Blueprint. All Rights Reserved.