Tailoring Decks for Angel Investors vs. VCs (The Split Strategy)

Angels buy with emotion; VCs buy with calculators. A forensic audit on Tailoring Decks for Angel Investors vs. VCs: Why sending a 'Spreadsheet Deck' to an Angel is a deal-killer.

1.4 HOW PITCH DECKS FIT INTO DIFFERENT FUNDRAISING STAGES?

1/26/20264 min read

The Liquidity Bifurcation: Why "One Deck Fits All" Kills Your Cap Table

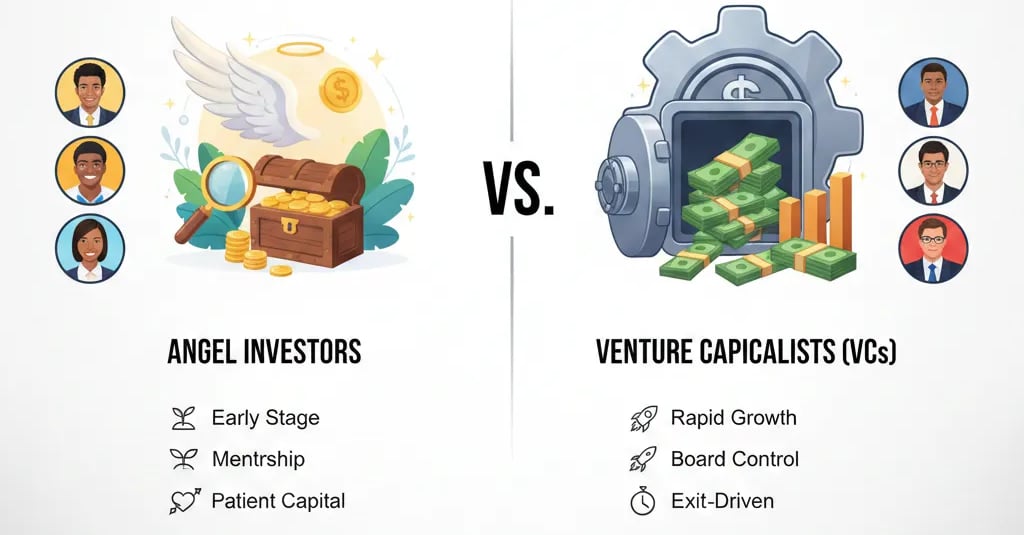

Founders often treat fundraising as a monolithic activity, blasting the same PDF to a retired dentist in Leeds and a General Partner at a Tier-1 firm on Sand Hill Road. This is capital suicide. Angels and VCs operate on fundamentally opposing risk curves. Angels buy the pilot; VCs buy the airline. Sending a metric-heavy, risk-adjusted Series A deck to an Angel triggers analysis paralysis. Conversely, sending a vision-heavy, "trust me" deck to a VC signals operational immaturity. This distinction is not a nuance; it is a foundational layer of How Pitch Decks Fit Into Different Fundraising Stages. If you cannot bifurcate your narrative based on the liquidity horizon of the recipient, you are not ready for institutional capital.

The "Red Flag" of Context Collapse

The most damaging error forensic auditors see in data rooms is Context Collapse: a single deck trying to serve two masters with opposing psychological drivers.

The "Red Flag" Scenario: You present a slide detailing a complex 5-year financial model with projected EBITDA margins to an Angel Investor.

The Angel thinks: "This looks like a job. I’m investing $25k for the excitement and the founder’s grit. This spreadsheet proves nothing at pre-revenue."

The Result: The Angel disengages because the emotional hook is buried under administrative weight.

Conversely, you show a slide emphasizing "Mission, Passion, and Story" with zero unit economics to a Series A VC.

The VC thinks: "This is a lifestyle business. They don't know their CAC, they don't understand burn multiples, and they are hiding operational incompetence behind a 'vision'."

The Result: Immediate pass. The VC has a fiduciary duty to LPs to deploy capital into scalable machines, not passionate projects.

Psychological Audit: Founders commit this error due to Efficiency Bias. You believe a single "master deck" saves time. In reality, it ensures rejection from both sides. You are optimizing for your convenience, not the investor's specific thesis.

The Power Law vs. The Passion Bet

The logic for tailoring decks is rooted in the Expected Value (EV) equation of the investor class.

Angel Math (The 10x Target):

Angels invest their own net worth.

Check Size: $10k - $100k.

Target: 3x-10x return.

Mechanism: They bet on the Founder's Character + Market Inefficiency.

Cognitive Load: If they have to do math to understand why you win, you lose. They need visceral confirmation.

VC Math (The Power Law):

VCs invest OPM (Other People's Money).

Check Size: $2M - $10M (Series A).

Target: The fund needs one company to return the entire fund (100x+).

Mechanism: They bet on Unit Economics + Moat.

Cognitive Load: They need proof of scalability. Every slide without a number is wasted real estate.

The Divergence Logic:

Input: Angel Capital = High Emotion / Lower Due Diligence.

Input: VC Capital = Low Emotion / Forensic Due Diligence.

Conclusion: A deck optimized for "High Emotion" (Angels) fails the "Forensic" test (VCs). A deck optimized for "Forensic" data (VCs) kills the "Emotion" (Angels).

The Bifurcated Narrative

Stop sending the same file. You need two distinct assets in your data room.

Asset A: The Angel Deck (The "Belief" Asset)

Focus: The Problem, The Solution, The Founder.

Tone: Narrative-driven, visionary, urgent.

Key Metric: Early traction (waitlists, beta users) and "Why Now."

The Slide: The "Team" slide takes prominence. Show why you are the only person who can solve this.

Weak Version: "We have 10 years of combined experience."

Angel-Ready Version: "Ex-Google Lead and PhD in AI; we built this specifically because we saw X market failure firsthand."

Asset B: The VC Deck (The "Scale" Asset)

Focus: The Market Size (TAM), Unit Economics, The Exit.

Tone: Clinical, precise, inevitable.

Key Metric: LTV:CAC > 3:1, Net Dollar Retention (NDR) > 100%, Burn Multiples < 2x.

The Slide: The "GTM (Go-to-Market) Strategy" slide is mandatory.

Weak Version: "We will use ads and social media."

VC-Ready Version: "Current CAC is $45 via LinkedIn InMail. LTV is $2,500. Payback period is 4 months. $2M injection scales ad spend to achieve $5M ARR in 18 months based on current conversion rates."

The Framework: Use the "Risk-Reward Inversion".

For Angels, highlight the Reward (Vision). Minimize the perception of technical risk.

For VCs, highlight the mitigation of Risk (Execution). Prove the reward is mathematically inevitable if execution holds.

The "Death Traps"

The "Hybrid" Frankendeck: Founders try to merge both styles, resulting in a 25-slide monster. It is too long for an Angel to read and too fluffy for a VC to respect.

Timing Mismatch: Showing a VC-style "Exit Strategy" slide to an Angel too early makes you look like a mercenary looking for a quick flip, rather than a builder.

The "SAFE" Confusion: Do not pitch an Angel using complex Series A structural terms (e.g., participating preferred shares) unless they are sophisticated. Stick to simple SAFEs or Convertible Notes for Angels; reserve the heavy legal structuring for the VC Term Sheet.

Conclusion

Tailoring your deck isn't about changing the truth; it's about translating your business into the correct currency of risk. For Angels, that currency is faith. For VCs, that currency is data. Correctly bifurcating your assets increases your conversion rate at both stages, preventing the "uninvestable" label that sticks to founders who don't understand their audience. This strategic segmentation is the core of How VC Pitch Decks Really Work in 2026 — And Why Most Founders Get Them Wrong.

You can build these distinct narratives manually, or use The Slide-By-Slide VC Instruction Guide included in our $5k Consultant Replacement Kit ($497) available on the home page. It contains the exact architectural blueprints to clone for both Angel and Institutional raises.

Funding Blueprint

© 2026 Funding Blueprint. All Rights Reserved.