Slide-by-Slide Mastery: How VCs Evaluate Every Pitch Deck Slide

Discover how VCs actually evaluate every pitch deck slide. Learn the forensic framework, traction metrics, and red flags that kill 97% of startup decks.

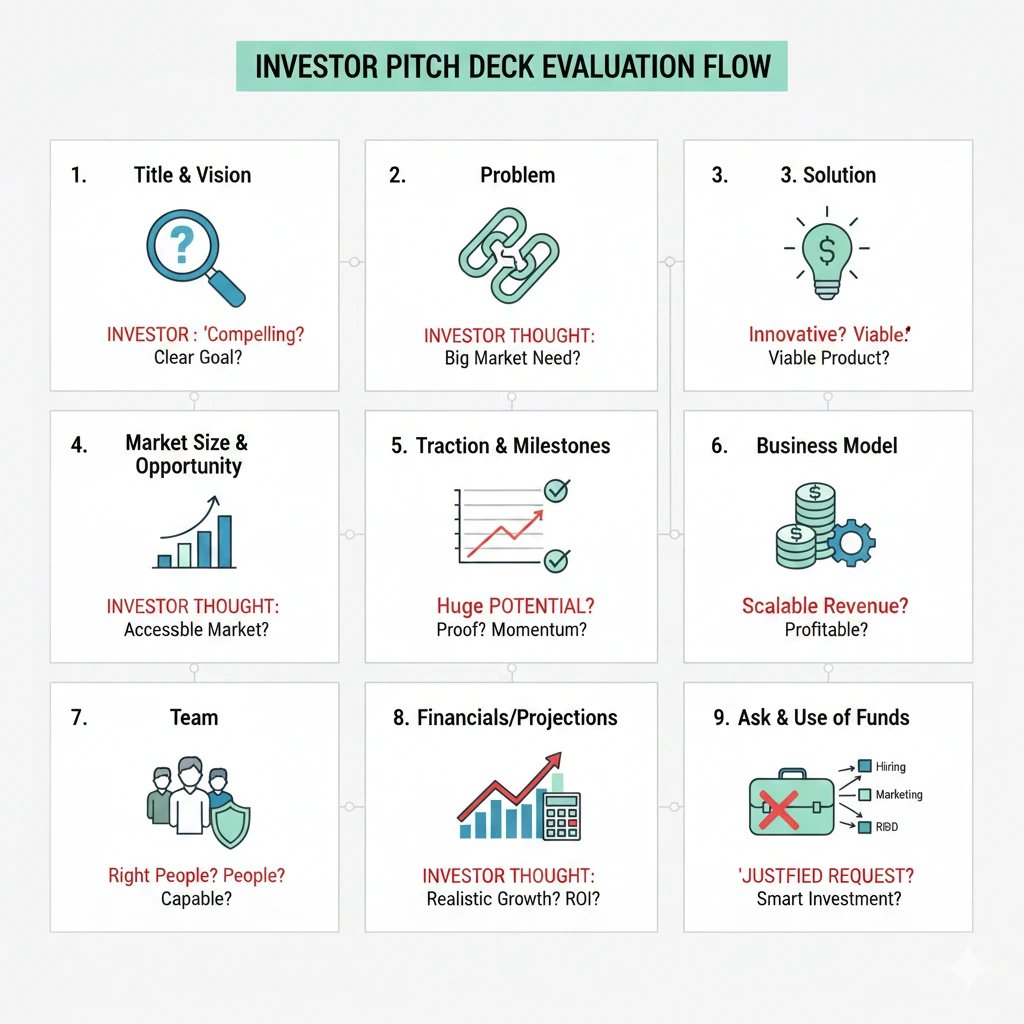

PILLAR 3: SLIDE STRUCTURE & FRAMEWORKS

12/15/20251 min read

Deep Dives: Slide-by-Slide Mastery: How VCs Evaluate Every Pitch Deck Slide

Pitch Deck Problem Slide: How to Build Urgency for VCs

Pitch Deck Solution Slide: Presenting a Scalable Startup

Pitch Deck Market Slide: Proving Total Addressable Market (TAM)

Pitch Deck Business Model Slide: Showing VCs How You Make Money

Pitch Deck Traction Slide: Proving Progress at the Early Stage

Pitch Deck Competition Slide: Positioning Against Startup Rivals

Pitch Deck Financials Slide: Presenting Projections VCs Trust

Pitch Deck Team Slide: Proving Founder-Market Fit to Investors

Pitch Deck Ask Slide: Structuring Funding Needs & Use of Funds

Funding Blueprint

© 2026 Funding Blueprint. All Rights Reserved.