How Pre-Seed Decks Differ From Seed Decks: Why Founders Fail the Maturity Test

Pre-Seed is a promise; Seed is proof. A forensic audit on the Maturity Test: Why using a 'Vision Deck' for a 'Traction Round' triggers an automatic rejection.

1.4 HOW PITCH DECKS FIT INTO DIFFERENT FUNDRAISING STAGES?

1/24/20264 min read

The Pre-Seed vs. Seed Delusion: Why Founders Fail the Maturity Test

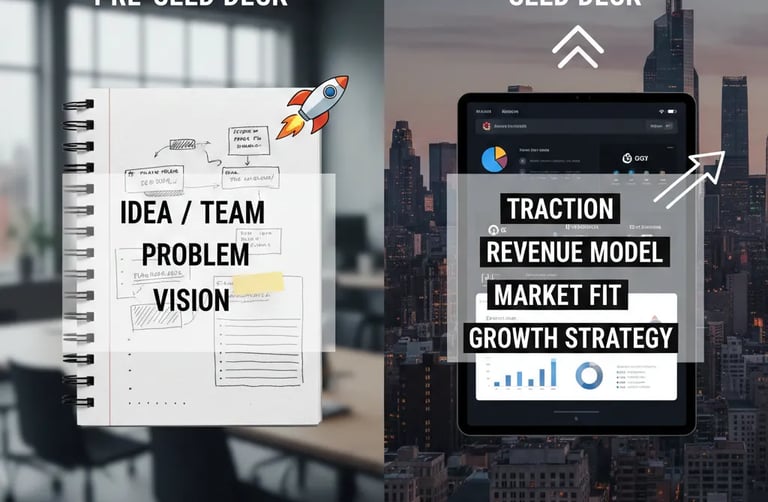

Most founders treat a Seed round as "Pre-Seed but with more traction." This is a $2 million mistake. If you walk into a Seed meeting with a Pre-Seed narrative, you aren't just early; you are incompetent. This distinction is part of a foundational layer in your capital strategy, detailed in How Pitch Decks Fit Into Different Fundraising Stages. At Pre-Seed, you are selling a possibility—a bet on founder-market fit and a massive TAM. By the Seed stage, the VC is no longer buying your vision; they are buying your unit economics and a repeatable customer acquisition engine. If you can’t articulate the shift from "we think" to "we know," you are dead on arrival.

The Forensic Diagnosis

The most common point of failure is "Narrative Inertia." Founders spend 12 months in the trenches at Pre-Seed, perfecting a deck that emphasizes the "Problem" and "Team." When they go to raise a Seed, they simply update the traction slide and change the "Ask" from $500k to $3M.

The Red Flag Scenario: A Seed-stage deck that devotes 40% of its real estate to the "Problem" slide. To a Series A analyst or a sophisticated Seed fund in London or Silicon Valley, this signal is clear: The founder hasn't found product-market fit (PMF). If you are still trying to prove the problem exists at the Seed stage, it means your data isn't strong enough to let the solution speak for itself.

Psychological Audit: Founders cling to Pre-Seed narratives because of Intellectual Cowardice. It is safer to talk about a "trillion-dollar opportunity" than to explain why your Month 3 retention is at 40% when the industry standard is 60%. They hide behind "Vision" because they are afraid of the "Forensic Reality" of their own metrics.

The Mathematical Proof / The "Why"

The transition from Pre-Seed to Seed is a shift in the Risk Profile.

Pre-Seed Risk: Technical and Team. Can they build it? Are they the right people?

Seed Risk: Distribution and Scalability. Can they sell it at a cost that doesn't bankrupt the company?

Consider the Cognitive Load of a VC. They spend an average of 190 seconds on a deck. If 120 of those seconds are spent on "Market Opportunity" (Pre-Seed focus), you have only 70 seconds left to prove your Burn Multiple and LTV/CAC ratio.

Efficiency over Hope: At Pre-Seed, a Burn Multiple of 3.0x is ignored. At Seed, if your Burn Multiple (Net Burn / Net New ARR) is above 2.0x, you are viewed as an inefficient operator.

The Dilution Math: Seed investors are looking for a 15-25% stake. They calculate your "Exit Velocity." If your Seed deck doesn't show a clear path to $1M ARR within 12 months, your valuation will be crushed by "Risk Weighting."

The 3:1 Ratio: At Pre-Seed, your CAC is an estimate. At Seed, if your LTV/CAC isn't trending toward 3:1 with a payback period under 12 months, you don't have a business; you have a subsidized hobby.

The "Insider" Solution Protocol

To survive the transition, you must audit your deck for Technical Maturity. You are moving from a Delaware C-Corp concept to a Silicon Valley execution machine.

The Before vs. After

Weak Pre-Seed Slide: "Our market is $100B and we have a waitlist of 5,000 people." (Focus: Breadth/Potential)

VC-Ready Seed Slide: "Our CAC is $45 across Meta and LinkedIn, yielding a $150 ACV. With $2M in Seed funding, we scale these proven channels to hit $1.2M ARR in 14 months." (Focus: Depth/Predictability)

The Execution Framework: The "Seed Maturity Equation"

Use the "Efficiency Score" to validate your Seed readiness:

Net New ARR / Total Capital Burned > 0.5.

Step-By-Step Fix:

Kill the "Vision" Fluff: Reduce your "Problem" and "Market" slides to a combined two-slide maximum.

The "Engine" Slide: Insert a slide titled "Customer Acquisition Engine." This must detail your primary, secondary, and tertiary distribution channels with specific, audited costs.

The Milestone Bridge: Don't just list "Hiring Engineers" as a use of funds. Map every dollar of the Seed round to a specific valuation inflection point for Series A.

The "Death Traps"

The 2021 Carryover: Founders still try to raise Seed rounds based on "User Growth" alone. In 2026, Revenue is the only metric that isn't a lie. If you aren't showing a path to monetization, you aren't a Seed company.

Over-Correcting on Profit: While efficiency matters, Seed is still about growth. Don't pitch a "Lifestyle Business" that achieves profitability too early at the expense of market capture. VCs want Aggressive Efficiency, not cautious stagnation.

Using Regional Terminology: If you are pitching a NYC or London fund, do not use local slang or niche geographic metrics. Stick to the "Global VC Standard" of ARR, MRR, and Churn.

The "High-Ticket" Conclusion

Reframing your deck from Pre-Seed "Hope" to Seed "Execution" is the difference between a 10% and a 30% conversion rate on your partner meetings. Investors do not fund ideas at the Seed stage; they fund systems. Correcting your narrative maturity can easily add $1M to $3M to your pre-money valuation by removing the "Execution Risk" discount.

This protocol is a single component of the How VC Pitch Decks Really Work in 2026 — And Why Most Founders Get Them Wrong.

The Filter: You can attempt to bridge this gap manually, or use the Slide-By-Slide VC Instruction Guide included in our $5k Consultant Replacement Kit ($497) available on the home page. It automates the transition from "Visionary" to "Operator" so you don't get laughed out of the boardroom.

Would you like me to generate the Forensic Image Prompt for this post to maintain the "Finance-Noir" aesthetic?

Funding Blueprint

© 2026 Funding Blueprint. All Rights Reserved.