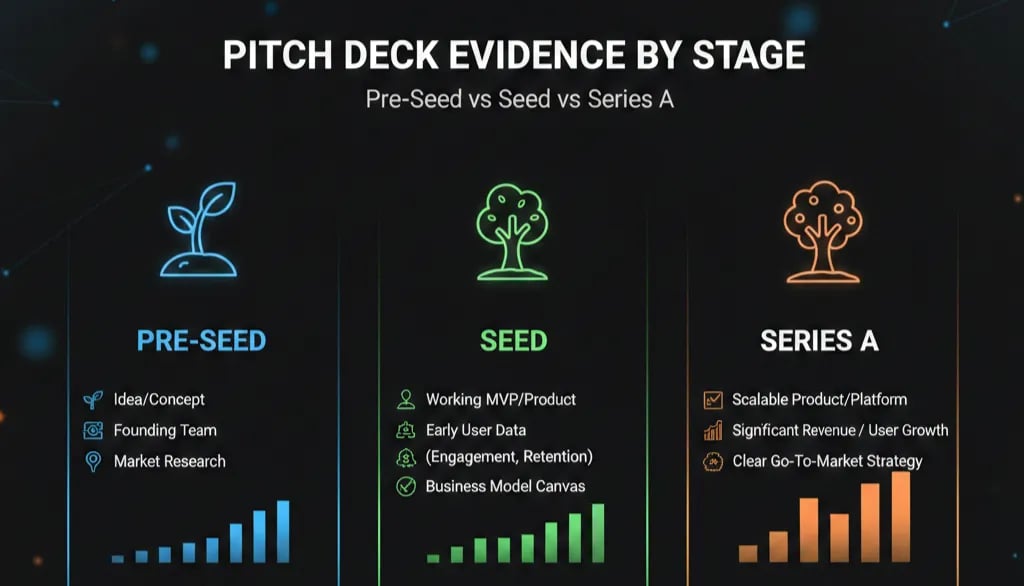

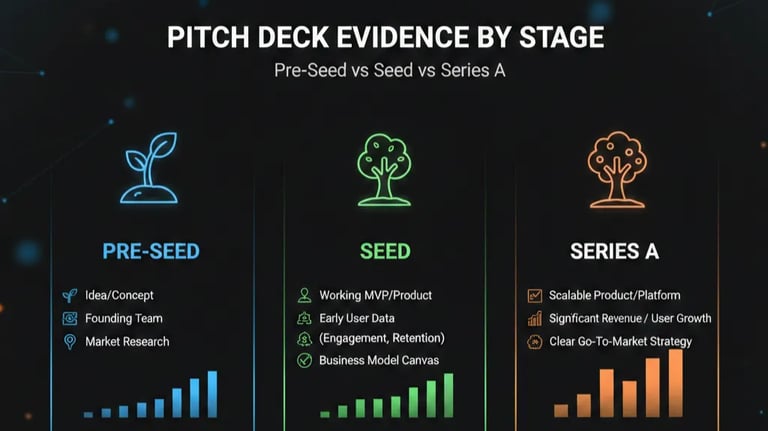

Pitch Deck Evidence by Stage: Pre-Seed vs Seed vs Series A

Is your pitch deck pretending to be a stage it isn't? Stage-mismatched evidence kills rounds. Learn what VCs actually require at Pre-Seed, Seed, and Series A.

2.5 PROBLEM/SOLUTION SLIDES BY STAGE: PRE-SEED → SEED → SERIES A

2/21/20264 min read

What Evidence Your Pitch Deck Actually Needs at Pre-Seed, Seed, and Series A (And Why Mixing Them Kills the Round)

$0 in revenue. $180K in MRR. $2.1M in ARR. Three founders. Three decks. All three lost the round — not because the business was wrong, but because the evidence on their Problem and Solution slides did not match the stage they were raising for.

This is the single most consistent structural error in early-stage fundraising, and it compounds because it looks like a content problem when it is actually a logic problem. Fixing the copy does not fix it. This is part of a deeper framework — you can read the full breakdown of how Problem and Solution slides work at each funding stage before continuing here.

Why Stage-Mismatched Evidence Is a Silent Round-Killer

VCs are not reading your slides. They are running a rapid risk-scoring model against whatever mental checklist their fund mandate requires at that moment. A Pre-Seed partner is asking: "Is this a real problem and does this team have uncommon insight into it?" A Series A partner is asking: "Has this been validated at scale, and does the unit economics confirm the business model is not a coincidence?"

When you put the wrong type of evidence on the slide — anecdotes at Series A, or revenue projections at Pre-Seed — the VC does not conclude that you are enthusiastic. They conclude that you do not understand where you are. That is a founder judgment failure, and it ends the meeting faster than a bad market size.

The psychological driver here is stage anxiety. Founders at Pre-Seed try to look like Seed. Seed founders try to look like Series A. The result is a deck that satisfies no one because it is pretending to be something it is not. In a deck reviewed last quarter, a B2B SaaS founder included three customer logos and a burn multiple on a Pre-Seed raise — the VC passed at slide 4, citing "unclear on where they actually are." The logos were real. The problem was framing.

Investors are not rewarding ambition when they see mismatched evidence. They are identifying a founder who does not know how to read the room — and that is a pattern that does not improve post-check.

The Stage-Evidence Matrix: What Each Round Actually Requires

Here is the logic mapped precisely. The evidence type must match the risk profile of that stage — nothing more, nothing less.

Pre-Seed Problem Slide — Evidence Required:

Qualitative insight: 15–30 direct founder interviews (named industries, not named companies)

A clear articulation of why now this problem is worse than 3 years ago

Founder proximity to the problem (domain authority, not a pivot story)

Pre-Seed Solution Slide — Evidence Required:

A working hypothesis with a clear mechanism

Optionally: an MVP interaction, waitlist size, or pilot LOI

NOT: revenue, retention data, or CAC

Seed Problem Slide — Evidence Required:

Quantified pain: "We spoke to 60 ops leads. 47 said X cost them $80K–$150K annually."

Early market signals: waitlist conversion, pilot MRR ($5K–$50K is acceptable)

One or two reference customers who can be called

Seed Solution Slide — Evidence Required:

Proof of mechanism: why your approach works where others fail

Early retention signal: even 60-day cohort data

NOT: projections dressed as evidence

Series A Problem Slide — Evidence Required:

As of 2025, median Series A pre-money in the US sits at $22M–$28M; at that valuation, the VC's LP base demands market evidence, not founder conviction

Quantified market pain with third-party corroboration (industry report, named analyst, or public dataset)

Demonstrated via your own cohort: "We see this problem cost our customers $X on average, validated across 80 paying accounts"

Series A Solution Slide — Evidence Required:

Retention curve at 12+ months

NRR above 110% (120%+ is expected by top-tier funds)

CAC payback under 18 months

NOT: case studies without numbers attached

The pattern is not complexity — it is specificity calibrated to what the VC can verify at each stage.

The Before/After Fix: What "VC-Ready" Evidence Actually Looks Like

Weak Version (Pre-Seed founder, Seed deck framing):

"The market for supply chain software is $47B. Our solution reduces waste by 30%. Early customers love it."

This is three unsubstantiated claims dressed as evidence. It fails at every stage.

VC-Ready Version (Pre-Seed):

"We interviewed 22 warehouse ops managers across mid-market 3PL firms. 18 cited manual reconciliation as their top daily drain — averaging 3.4 hours per shift. No current tool addresses the sub-$5M 3PL segment."

Use the Evidence Ladder Framework to construct each slide:

Source — Who told you this, and how many?

Specificity — A number, not an adjective

Mechanism — Why does your solution fix this specific version of the problem?

Stage-Appropriate Proof — Qualitative (Pre-Seed), Early Quantitative (Seed), Scaled Quantitative (Series A)

At no stage does "customers love it" count as evidence. Love does not appear on a cap table.

For Series A, apply the Retention-as-Evidence Rule: NRR × Cohort Depth = Credibility Score. If your NRR is 115% but you only have 6-month cohorts, you do not have Series A evidence. You have Seed evidence with optimistic extrapolation. VCs know the difference.

Four Stage-Evidence Errors That Survive the First Rewrite

1. Upgrading language without upgrading proof. Swapping "users love it" for "strong retention metrics" without showing the actual curve. Analysts will ask. You will not have the answer.

2. Using 2021-era growth benchmarks to frame your Series A. Top-tier US funds in 2026 are stress-testing 18-month minimum runways and expect burn multiples below 1.5x at Series A. A deck built on 2021 growth-at-all-costs framing reads as a founder who has not updated their model.

3. Mixing stage evidence on the same slide. A Pre-Seed founder who puts "projected ARR" next to qualitative customer quotes is telling two different stories. The VC reads contradiction, not ambition.

The Evidence Gap Is a Valuation Gap

Fixing stage-evidence alignment is not cosmetic. A misaligned Problem slide suppresses your pre-money because it forces the VC to mentally discount everything that follows. When the evidence matches the stage, the narrative becomes self-reinforcing — and a self-reinforcing deck commands a higher anchor in the term sheet negotiation.

The full system for building slides that survive due diligence — at every stage — is inside the complete Problem and Solution slide framework for venture-backed founders. That is where the architecture lives.

Founders who have used the Slide-By-Slide VC Instruction Guide inside the $5K Consultant Replacement Kit go into partner meetings with evidence structures that already match what the VC's analyst will cross-check during diligence. At Pre-Seed, Seed, and Series A, the bar is different — and the Guide is built to the correct bar for each. That is not a marginal edge; it is the difference between a resubmit and a term sheet. The full Kit is $497. Access it at the stage-specific pitch deck system built for serious founders.

The round you are raising is not about how good the business is. It is about whether your evidence speaks the language of the capital you are asking for.

Funding Blueprint

© 2026 Funding Blueprint. All Rights Reserved.