The Stage-Adaptive Pitch Deck: A Framework for Pre-Seed to Series A

Is your pitch deck too thin for Series A or too heavy for Pre-Seed? Stop using static documents. Learn why the Stage-Adaptive Framework secures term sheets.

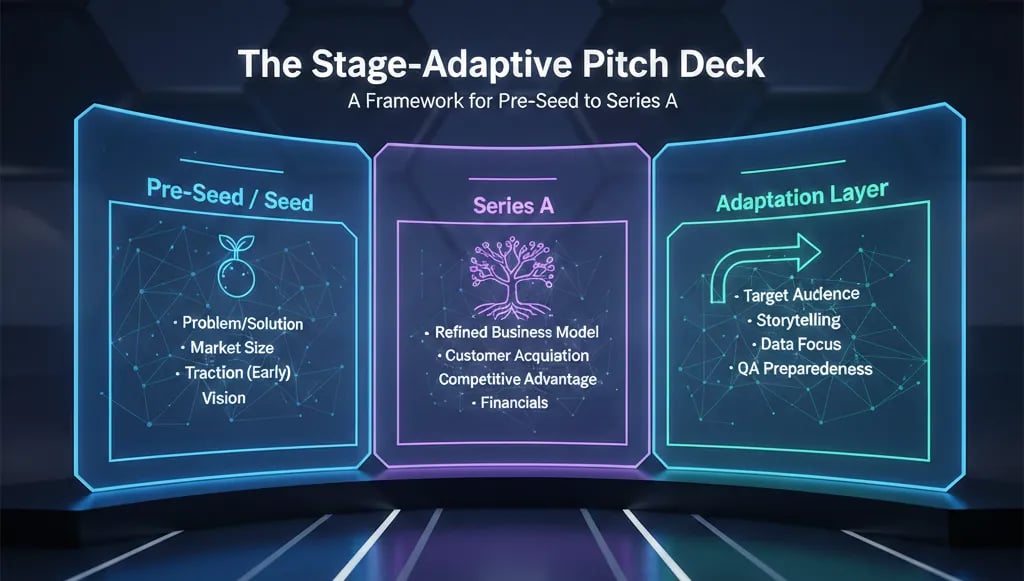

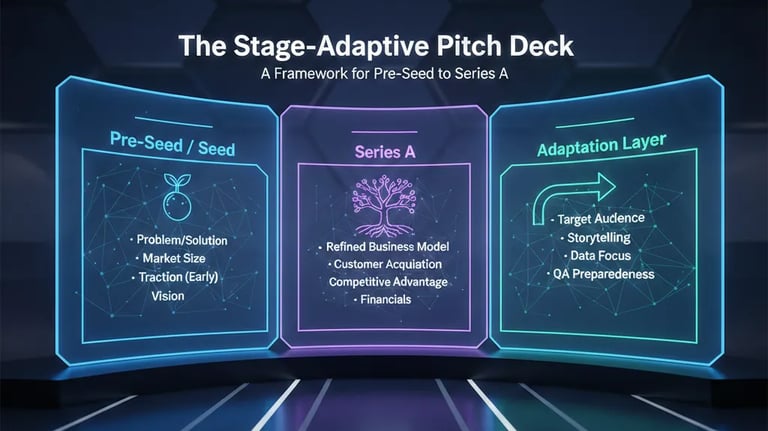

2.5 PROBLEM/SOLUTION SLIDES BY STAGE: PRE-SEED → SEED → SERIES A

2/23/20269 min read

The Stage-Adaptive Pitch Deck: A Framework for Pre-Seed to Series A

Most founders treat their pitch deck as a document. The ones who consistently close rounds treat it as a dynamic instrument that is recalibrated for every stage of capital, every investor psychology, and every shift in the market environment they are raising into. The distinction sounds philosophical. The financial consequences are not. A static document pitched across three rounds fails twice — once when it is too thin for the stage being targeted, and again when the founder cannot understand why a business with genuine traction keeps hearing "not quite yet." Both failures are architectural, not commercial, and both are preventable with a framework that treats the deck as something that must adapt rather than something that must simply grow. That adaptive logic is the structural foundation of the Problem and Solution Slides stage-specific framework from Pre-Seed through Series A — and this post operationalises it into a complete, stage-by-stage system a founder can deploy before their next process opens.

Why a Single Deck Architecture Cannot Serve Three Fundamentally Different Capital Conversations

The assumption embedded in most pitch deck advice is that a great deck is a great deck — that quality, clarity, and a compelling narrative translate across stages. That assumption collapses the moment you understand what the investor is actually purchasing at each round.

At Pre-Seed, the investor is purchasing a thesis bet. They are backing a founder's ability to see a non-obvious problem clearly enough to build a solution worth funding. The deck's job is to make that thesis legible, credible, and specific. Evidence is secondary to perception of intellectual sharpness and founder-market fit.

At Seed, the investor is purchasing a demand proof. They are backing early evidence that a real market exists — that buyers have responded to the problem with financial behaviour, not just conversational agreement. The deck's job is to prove that the hypothesis has made contact with reality and survived that contact.

At Series A, the investor is purchasing a revenue system. They are backing a documented, repeatable mechanism for acquiring, retaining, and expanding a specific customer segment — and they are doing so with a check that requires the mechanism to be operating, not planned. The deck's job is to prove that the business has learned from its customer base and translated that learning into a scalable commercial architecture.

These are not variations of the same conversation. They are categorically different capital decisions requiring categorically different decks. A framework built for one stage will actively misrepresent the business at another — and in a post-2023 fundraising environment where, as of early 2026, US Series A processes at top-tier funds are running 10–14 week diligence timelines with structured ICP audits as standard, misrepresentation is identified faster and penalised harder than at any point in the last decade.

The three-stage architecture problem requires a three-stage solution. Here is the complete framework.

The Stage-Adaptive Framework: Structural Logic for Every Layer of Your Deck

The framework operates on a single governing principle: every slide in a stage-adaptive deck must answer the primary investment question of that specific stage before it answers anything else. Secondary information — market size, team credentials, product features — is only credible after the primary question is answered. Founders who reverse this order, leading with what impresses rather than what the investor needs to resolve first, create decks that feel strong and perform poorly.

Here is the primary investment question by stage, followed by the structural adaptation required to answer it:

Pre-Seed Primary Question: "Do I believe this founder has found something real?"

The structural implication for your Problem slide: it must open with the discovery mechanism, not the problem description. How did you find this problem? What made you look where others had not? The insight origin is the credibility signal at Pre-Seed — not the market size, not the product vision, not the founder credentials. Those elements support the answer. They are not the answer.

Adaptive structure for the Pre-Seed Problem slide:

Sentence 1: The specific buyer type, named precisely.

Sentence 2: The specific behaviour or failure mode that revealed the problem — not the problem as a category, but the observable symptom that a founder who had done primary discovery would know.

Sentence 3: Why existing solutions fail this buyer, stated in the buyer's economic terms.

What to exclude: Market size statistics, revenue projections, and competitive landscape slides that imply more certainty than a Pre-Seed business has earned. A TAM slide at Pre-Seed is almost always top-down, theoretical, and read by investors as a signal that the founder is performing scale rather than demonstrating insight.

Seed Primary Question: "Have real buyers confirmed this problem is worth solving?"

The structural implication for your Problem and Solution slides: both must operate in the language of buyer behaviour, not founder observation. The shift is subtle and critical. "Buyers struggle with X" is founder observation. "Our 34 pilot customers were paying an average of $1,400 per month for an inferior workaround before switching" is buyer behaviour. One describes. The other proves.

Adaptive structure for the Seed Problem slide:

Evidence anchor: A quantified cost of the problem in the buyer's own financial terms — time, money, or error rate — derived from your actual conversations or pilot data, not industry reports.

Segment lock: The problem must be attributed to a named, specific buyer type. Not "SMBs" or "mid-market companies." The job title, company stage, and operating context of the human who experiences the pain.

Workaround reference: What the buyer is currently doing to manage the problem. This is the single most powerful validation signal on a Seed-stage Problem slide, because a documented workaround proves the problem is real enough to generate financial behaviour without your product existing.

Adaptive structure for the Seed Solution slide:

Lead with the outcome the buyer achieves, stated in the same financial terms as the problem. If the problem cost $1,400 per month, the solution must reference what that $1,400 is replaced by — not what features your product has.

Reference the mechanism only after the outcome. The VC needs to believe the outcome is real before they care about how you deliver it.

Series A Primary Question: "Can this business repeat its early wins without the founder in the room?"

This is the question that recycled Seed decks fail to answer — and failing to answer it is the architectural error that produces the "we love the traction but aren't yet convinced" rejection pattern. The Series A Problem and Solution slides must be rebuilt around earned commercial intelligence, not validated demand. The distinction is material.

I have seen this specific failure in seven Series A processes over the past eight months — a founder presents a Solution slide built around product capability and early customer wins, with no documented evidence of a sales motion that operates independently of founder involvement. The partner meeting ends with questions about the sales team that the deck was never structured to answer.

Adaptive structure for the Series A Problem slide:

ICP refinement statement: The named buyer segment you started with versus the named buyer segment your retention data has confirmed as your actual best customer. If those two are the same, you have not done the analysis. Eighteen months of customer data should have sharpened the original ICP, not confirmed it unchanged.

Cohort-level problem differentiation: Which segment of your customer base experiences the problem most acutely, and how does that correlate with your NRR? The Problem slide at Series A must connect problem intensity to revenue quality. High-NRR cohorts exist because the problem is more acute for them — your slide must make that connection explicit.

Competitive evolution acknowledgement: What has changed in the competitive landscape since your last raise? A Problem slide that does not acknowledge the current competitive context reads as disconnected from market reality.

Adaptive structure for the Series A Solution slide:

GTM repeatability proof: Not "we sell to mid-market ops teams" but "we acquire mid-market ops teams through outbound sequences targeting VP Operations hires in the first 90 days post-funding, at a CAC of $4,200 and a payback period of 7 months, executed by a two-person SDR team without founder involvement."

Expansion architecture: How does the solution grow within a customer account? NRR above 110% at Series A is table stakes at top-tier funds. The Solution slide must show the mechanism that drives it — not just report the number.

Channel specificity: Every revenue channel documented separately, with CAC and conversion rate by channel. Blended CAC at Series A is a red flag. It signals the founder cannot identify which acquisition motion is actually working.

The Adaptive Deck Calibration Checklist: A Pre-Process Audit Tool

Before any deck goes to an investor at any stage, run it against this calibration checklist. Every "no" answer is a structural gap that will generate a diligence question the deck was not built to survive.

Pre-Seed Calibration:

Does the Problem slide open with a discovery mechanism rather than a problem description? (Yes / No)

Is the buyer named at the job-title level, not the company-type level? (Yes / No)

Is the problem framed in the buyer's economic language, not the founder's product language? (Yes / No)

Does the deck exclude market size claims that require certainty the business has not earned? (Yes / No)

Seed Calibration:

Does the Problem slide reference a quantified cost of the problem from actual customer or prospect data? (Yes / No)

Is there a documented workaround that proves buyer behaviour without your product? (Yes / No)

Does the Solution slide lead with outcome, not feature? (Yes / No)

Is the buyer segment specific enough that a VC could name one company that fits it without guessing? (Yes / No)

Series A Calibration:

Does the Problem slide show ICP refinement from original hypothesis to retention-data-confirmed segment? (Yes / No)

Is the problem intensity connected to NRR by cohort? (Yes / No)

Does the Solution slide document a GTM motion that operates without founder involvement? (Yes / No)

Is CAC reported by channel, not blended? (Yes / No)

Does the deck reflect competitive landscape evolution since the last raise? (Yes / No)

A deck that passes all calibration checks for its stage is not a guarantee of a term sheet. It is a guarantee that the deck itself will not be the reason the process fails — which eliminates the most common and most controllable variable in a fundraise.

Four Framework Execution Errors That Produce an Adaptive Deck That Still Fails

1. Applying Series A calibration criteria to a Seed-stage business. Founders who have read extensively about what Series A investors want sometimes build Seed decks with Series A structural requirements — cohort data, GTM channel separation, NRR by segment — against a customer base of 12 paying accounts. Thin data in a sophisticated structure is not impressive. It is transparently compensatory and raises questions about what the founder is hiding behind the complexity.

2. Treating the framework as a template rather than a logic system. The stage-adaptive framework is a set of structural principles, not a slide order. Founders who attempt to apply it by reorganising existing slide content without rebuilding the underlying evidence base will produce a deck with a new architecture and the same fundamental credibility gaps. The framework requires an evidence audit first, a structural rebuild second.

3. Adapting the Problem slide without adapting the Ask slide. The Ask slide — the raise amount, use of funds, and implied valuation — must also be stage-calibrated. A Seed-stage Ask slide on a Series A deck, or a Series A-sized raise request on a deck with Seed-stage evidence, creates an internal contradiction that collapses the credibility the adapted Problem and Solution slides worked to build. Every slide must communicate from the same stage register.

4. Running the calibration checklist once and treating it as permanent. The adaptive framework is a continuous operating practice, not a one-time pass. Market conditions shift, competitive landscapes evolve, and the ICP data from a growing customer base will contradict earlier assumptions. A deck that passed calibration six months ago may fail it today — and almost certainly will fail it at the next stage transition without a full rebuild.

The Raise You Lose to a Static Deck Is Not Recoverable

The stage-adaptive pitch deck framework is not a refinement exercise for founders who have almost everything right. It is the foundational architecture for every raise from the first check to the Series A close — because the raises that fail to static decks do not fail incrementally. They fail completely, consuming process time, burning warm introductions, and creating a market perception of a business that is raising but not closing. In a fundraising environment where reputational signal travels fast through investor networks, a failed process has a cost that extends beyond the round itself.

Founders who build stage-adaptive decks from the first draft do not just close faster. They enter each process from a position of structural credibility that changes the nature of the conversation — from "convince me this is real" to "let us discuss the terms of a business we both already believe in." That shift is the direct financial return on getting the architecture right.

For the complete system governing how Problem and Solution slides must be built, sequenced, and adapted at each stage — including the evidence standards, language tiers, and structural formats that underpin every framework element in this post — the full architecture is in the Problem and Solution Slides master guide.

Every week this framework is not deployed inside your deck is a week your slides are working against the raise your business deserves. The AI Financial System inside the $5K Consultant Replacement Kit applies the stage-adaptive framework directly to your financial narrative — calibrating your burn multiple presentation, your revenue architecture framing, and your Ask slide structure to the exact evidentiary standard your target stage demands, so your deck's financial layer matches the commercial intelligence your Problem and Solution slides are built to signal. The full Kit is $497, available at the stage-adaptive pitch deck system for Pre-Seed to Series A founders at FundingBlueprint.

Funding Blueprint

© 2026 Funding Blueprint. All Rights Reserved.