What Happens to Your Deck Once It Enters a VC Firm

You hit "Send" and get silence. Why? Because a 24-year-old Analyst just archived you to save "Political Capital." A forensic look at why you get ghosted and how to beat the "Junior Filter."

1.2: HOW INVESTORS USE PITCH DECKS INTERNALLY

1/17/20265 min read

The Autopsy of a "Pass": What Actually Happens Inside the Firm

Most Series A founders hallucinate a specific reality: they hit "send," a General Partner pours a scotch, reads every slide, and deeply contemplates the vision. This is delusion. Your deck is not literature; it is raw data entering a hostile algorithmic filter. If you are raising a Series A in 2026, you are likely failing the triage stage before a decision-maker ever sees your name. To understand why you are receiving silence instead of term sheets, you must understand the internal mechanics of the firm detailed in How Investors Use Pitch Decks Internally. If you do not optimize for the analyst's inbox, you are dead on arrival.

The Analyst "Kill Switch"

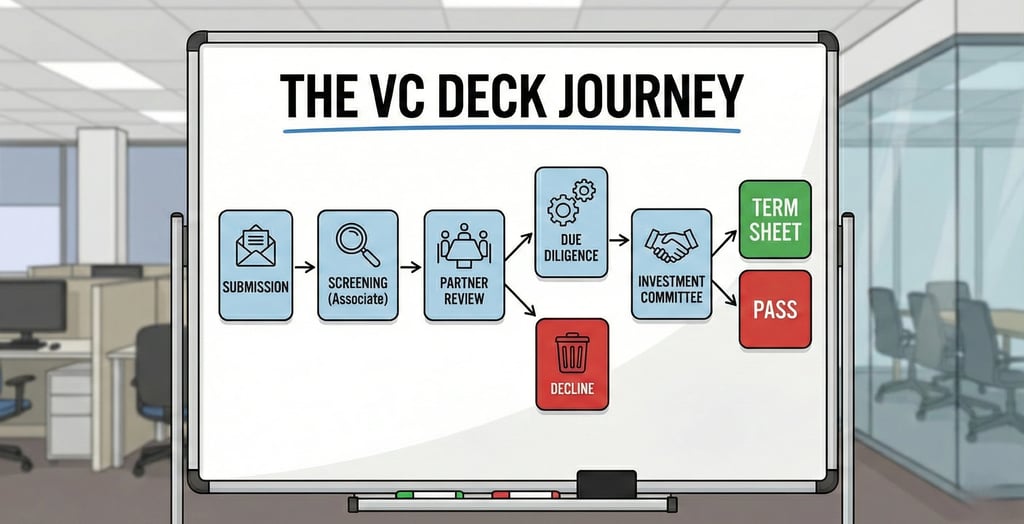

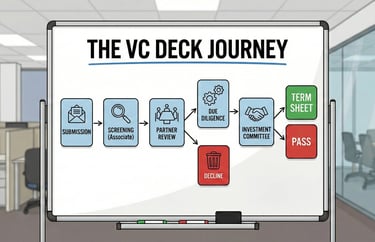

Here is the operational reality of a Tier-1 Venture Capital firm. Your deck does not go to the Partner. It lands in the inbox of a 24-year-old Associate or Senior Analyst who reviewed 50 other decks before lunch. Their job is not to find "good" deals. Their job is to not look stupid in front of the Partners.

The safest career move for an analyst is a "No." A "Yes" requires them to stake their limited political capital on your company. Therefore, they are looking for Disqualification Signals, not potential.

The "Red Flag" Scenario:

The analyst opens your deck. Slide 1 is a generic mission statement. Slide 2 is a "Problem" slide that describes a macro trend rather than a specific customer pain point. Slide 3 is a solution without a screenshot.

Analyst Thought Process: "Too abstract. High cognitive load. If I forward this, the Partner will ask for the CAC breakdown and it’s not here. I’m not wasting my political chips."

Result: The deck is archived. Time elapsed: 45 seconds.

Psychological Audit:

Founders build decks for "storytelling" because of bad advice from LinkedIn influencers who have never sat on an Investment Committee (IC). You are feeding your Ego, believing your narrative is so compelling it overrides metrics. You fear providing hard numbers because they look imperfect. The analyst interprets this omission not as "early-stage nuance," but as incompetence or deceit. You are trying to romance a calculator.

The Cognitive Load Equation

We can quantify the probability of your deck surviving the "Analyst Screen" using a simplified function of Cognitive Load (CL) and Signal Density (SD).

Every second an analyst spends trying to decipher what you actually do increases Cognitive Load. Conversely, every hard metric (Signal) reduces the risk of them looking foolish when they advocate for you.

The Internal Velocity Formula:

P(Meeting) = Signal Density X Time

Cognitive Load

Average Time Spent per Deck: 2 minutes, 42 seconds (DocSend data).

Average Time on "Financials" Slide: 23 seconds.

Average Time on "Team" Slide: 20 seconds.

If your "Solution" slide requires reading a paragraph of text (High CL) rather than glancing at a schematic (Low CL), your survivability drops by ~40%.

The Logic Chain of Rejection:

Ambiguity Tax: If the analyst has to read a sentence twice, you have lost. They assume you lack clarity of thought.

The "Partner Proxy" Test: The analyst mentally simulates the Partner asking: "What is their burn multiple?" If the answer isn't on Slide 8, the analyst has to email you to ask. That adds friction. Friction equals "Pass."

Pattern Matching Failure: VCs see 2,000 decks a year. They have a mental pattern for a "Series A SaaS Deck." If you deviate from the standard flow (Problem -> Solution -> Market -> Traction) to be "creative," you break the pattern match. You are now an anomaly, and anomalies are risky.

The bottom line: A confusing deck is mathematically indistinguishable from a bad business.

Writing for the Investment Memo

Stop writing a presentation. Start writing the Investment Memo for them.

The goal of your deck is to allow the analyst to copy-paste your slides directly into the internal Deal Memo they submit to the partnership. If you do their homework for them, you drastically increase your conversion rate from "Inbox" to "Partner Meeting."

The Protocol:

1. The "Headline" Thesis

Every slide headline must be a declarative assertion of value, not a label.

Weak Version: "Market Size." (This tells me nothing).

VC-Ready Version: "We are capturing a $4B SAM by displacing manual Excel workflows in Tier-2 Logistics." (This is the thesis).

2. The Metric anchor

Never present a qualitative claim without a quantitative anchor.

Weak Version: "We are growing fast."

VC-Ready Version: "Growing 15% MoM with a 3:1 LTV/CAC ratio."

3. The "2026" Unit Economics Framework

In 2021, you sold growth. In 2026, you sell efficiency. You must include a slide dedicated to Unit Economics that answers the "Rule of 40" or "Burn Multiple" questions immediately.

Use this specific Slide Structure for your Financials:

Top Left: ARR Growth. (Bar chart, last 12 months).

Top Right: Burn Multiple. (Burn / Net New ARR). Ideal is < 1.5 for Series A.

Bottom Left: CAC Payback. (In months). Ideal is < 12 months.

Bottom Right: NDR (Net Dollar Retention). Ideal is > 110%.

The Before vs. After:

The "Pass" Deck:

Slide 4 (Product): A list of features with generic icons. "We use AI to optimize workflows."

Analyst Reaction: "Vaporware. Everyone uses AI."

The "Meeting" Deck:

Slide 4 (Product): A split-screen visual. Left side: "Old Way (4 hours)." Right side: "Our Way (4 minutes)." A call-out box reads: "Client X reduced opex by 30% in Week 1."

Analyst Reaction: "Tangible ROI. I can defend this."

How to Fail While Trying to Fix It

Founders who attempt to optimize for the internal review often over-correct and fall into these specific traps:

The "Data Dump" Fallacy: You mistakenly believe "more data = more insider." You cram an Excel sheet onto a slide in 8pt font. This spikes Cognitive Load again. Rule: One core metric per chart. If you need a spreadsheet, put it in the Appendix.

The "2021 Valuation" Hangover: You anchor your ask based on revenue multiples from the ZIRP (Zero Interest Rate Policy) era. If you are asking for a $20M pre-money on $500k ARR in 2026, the analyst will not even finish the deck. They will close the tab because you are "market-illiterate."

The "Technobabble" Shield: Technical founders often hide business model weakness behind complex architecture diagrams. The IC doesn't care about your Kubernetes cluster yet; they care if anyone is paying for it.

The "High-Ticket" Conclusion

Optimizing your deck for the internal analyst is not about "design"; it is about capital efficiency. A deck that allows an analyst to write their memo in 20 minutes instead of 2 hours has a 5x higher velocity through the firm. In a Series A raise, speed is leverage. Fixing your narrative architecture to align with internal VC workflows can easily be the difference between a "pass" and adding $1M-$2M to your pre-money valuation due to increased competitive tension.

For the complete systemic breakdown of how to structure the rest of your raise, refer to How VC Pitch Decks Really Work in 2026 — And Why Most Founders Get Them Wrong.

The Filter:

You can attempt to reverse-engineer the internal VC memo manually, or you can use the Slide-By-Slide VC Instruction Guide included in our $5k Consultant Replacement Kit. It forces you to input the exact metrics analysts hunt for, effectively writing the investment memo for them. The kit is available for $497 on the home page. Do not let a solvable structural error cost you your round.

Funding Blueprint

© 2026 Funding Blueprint. All Rights Reserved.