How Your Deck Gets Compared With Other Startups in the Same Batch

You aren't a visionary; you are "Row 42." VCs process decks in batches, not vacuums. A forensic audit on why being "Comparable" kills your deal.

1.2: HOW INVESTORS USE PITCH DECKS INTERNALLY

1/20/20266 min read

You Are Not a Visionary; You Are Row 42 in a Spreadsheet

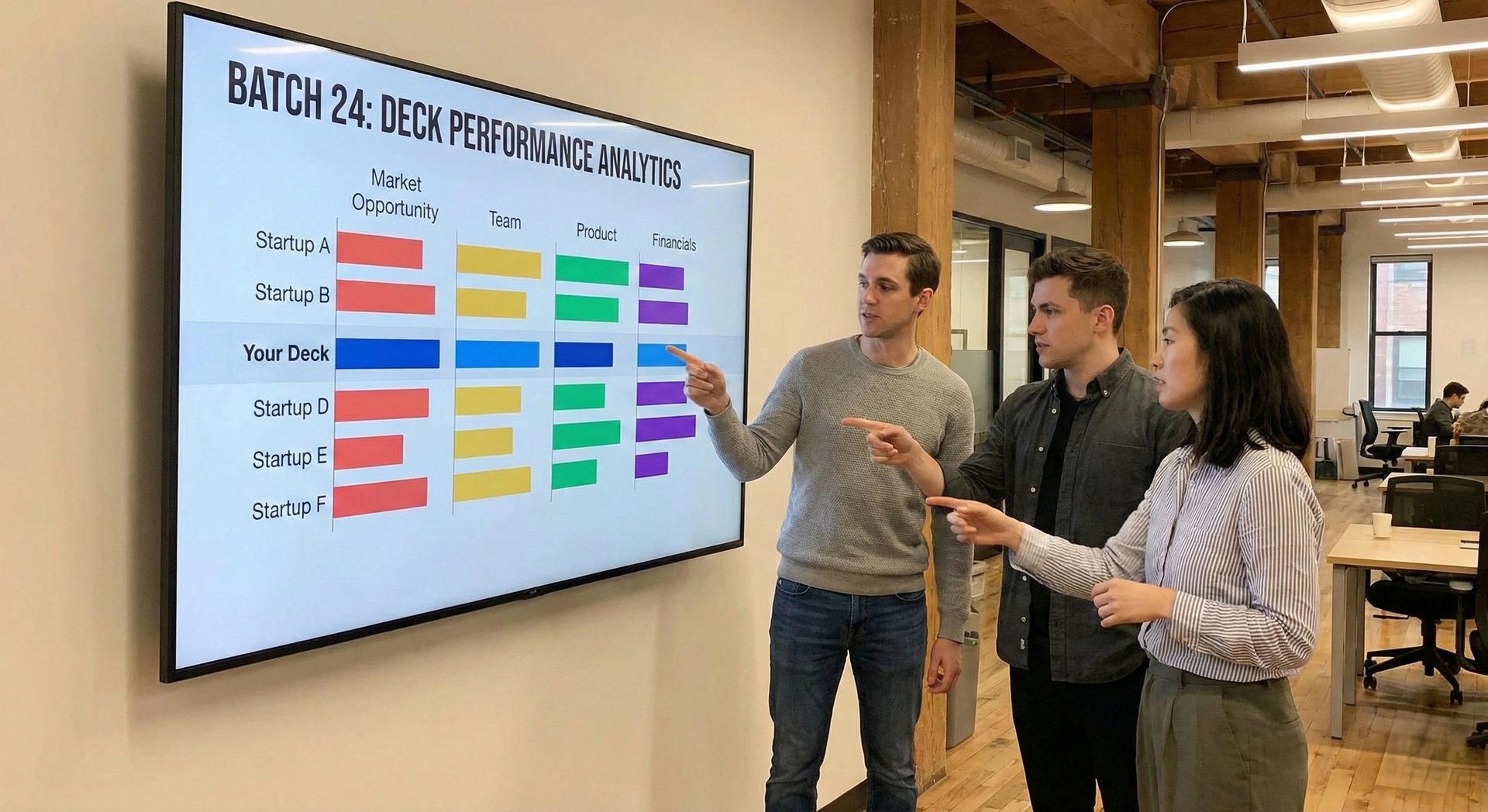

If you believe investors review your pitch deck in a vacuum of silence and focused contemplation, you are already dead in the water. The brutal reality of Series A fundraising is that your startup is rarely evaluated on its own merit; it is evaluated solely on its relative distance from the mean of the 50 other decks we received that week. You are not a unique snowflake; you are a data point in a batch processing queue. This is a critical distinction that separates the funded top 1% from the "promising but too early" masses. This concept is a foundational layer of How Investors Use Pitch Decks Internally, and ignoring it is effectively handing your term sheet to your competitor.

When a Junior Associate opens your deck, they are actively looking for reasons to archive it, not to fund it. Their job is to filter noise. If your deck looks, sounds, and models exactly like the three other "AI for Supply Chain" decks they saw before lunch, you are categorized as "Noise." You are instantly bucketed into a "Theme" (e.g., "Generative Sales Tools" or "Vertical SaaS for HVAC"). Once you are bucketed, you are no longer competing against the market; you are competing against the best company in that specific bucket right now. If you are not the clear outlier in that batch, you are simply market research for the eventual winner.

The "Index Match" Failure

The precise mechanism that destroys fundraises here is Cognitive Pattern Matching. VCs operate on pattern recognition to save time. When we see a batch of startups attacking the same problem space, we mentally (and often physically in our deal-flow CRMs like Affinity or Salesforce) group them.

The "Red Flag" Scenario

The fatal error occurs when your "Problem" and "Solution" slides use the exact same vernacular as the industry standard.

The Slide: A "Market Opportunity" slide stating, "The Logistics Industry is fragmented and inefficient," followed by a solution slide offering "An AI-powered dashboard for optimization."

The VC Internal Monologue: "I have seen this exact problem statement six times this month. This founder has no proprietary insight. They are building a consensus view of the market. Pass."

If your deck creates a sense of distinct familiarity, you have failed. Familiarity in venture capital does not breed comfort; it breeds contempt. It signals that you are following a trend rather than defining one.

The "Safety in Numbers" Fallacy

Founders make this mistake due to a psychological defect I call the "Safety in Numbers" Fallacy. You look at what other funded startups in your space are saying, and you mimic their language, thinking it validates your existence. You believe that sounding like a "standard" Series A company makes you investable.

This is false.

VCs are looking for variance, not conformity. You are signaling that you are a "Safe Bet," but venture returns are power-law distributed. We don't want safe bets; we want non-consensus, high-conviction outliers. By trying to fit in, you are structurally preventing yourself from standing out. You are optimizing for a "Maybe" instead of polarizing for a "Yes."

The "Alpha" vs. "Beta" Trap

Let’s strip the emotion and view your startup as an asset ticker.

In a batch of 20 similar decks (e.g., "GenAI for Legal"), the "Batch" itself represents the Market Beta (beta). These are the consensus features, standard pricing models, and average growth rates of the sector.

The VC Calculus:

LPs (Limited Partners) do not pay us management fees to buy Beta; they can buy a NASDAQ ETF for that. We exist solely to capture Alpha (alpha)—the idiosyncratic, excess return generated by your specific variance from the market.

Investment Probability (approx = ) Unique Insight (alpha)

Batch Correlation(beta)

If your deck mirrors the narrative, design, and metrics of the other 19 startups, your correlation to the batch is high (beta approx 1).

High Beta (Consensus): "We are doing what everyone else is doing, but better." - Uninvestable.

High Alpha (Divergence): "The entire batch is wrong about X; we are betting on Y."-Signal.

Statistically, if you look like the index, you are priced like the index. Since the "Index" of early-stage startups yields a negative return, you are priced at zero. We don't buy the bucket; we stock-pick the single asset that breaks the correlation.

The Cognitive Load Calculation

Consider the "Time to Rejection" metric.

Average time spent on a failed deck: 2 minutes, 40 seconds.

Average time spent on a 'Hot' deck: 6 minutes+.

Every slide that forces the investor to ask, "Wait, how is this different from Company X?" adds Cognitive Friction.

Slide 1 (Generic): +30 seconds of skepticism.

Slide 2 (Generic): +30 seconds of boredom.

Slide 3 (Generic): Archive.

You have a limited budget of "Mental Bandwidth" from the investor. If you spend that budget forcing them to compare you to others, you have no budget left to sell your unique vision.

High Signal-to-Noise Ratio: "We are the only company doing X using Y mechanism." (Immediate categorization as Unique).

Low Signal-to-Noise Ratio: "We are a better, faster, cheaper version of X." (Immediate categorization as Derivative).

The logic is binary:

If you are "Better," you are in a comparison war (metrics vs. metrics).

If you are "Different," you are in a category of one (monopoly dynamics).

VCs prefer Monopolies over Competitions.

The "Category of One" Framework

To escape the "Batch Comparison" death spiral, you must restructure your narrative to make comparison impossible. You do not want to be the "Best" option in the bucket; you want to destroy the bucket entirely.

Step 1: The "Anti-Positioning" Slide

Instead of waiting for the VC to compare you to competitors, pre-empt the comparison on Slide 2 or 3. Explicitly state why the current "Batch" of solutions fails.

Weak Version (Comparative): "We are 10x faster than Legacy Solution A and 50% cheaper than Competitor B."

Result: The VC opens a tab to check Competitor B’s pricing. You have invited diligence on your rivals.

VC-Ready Version (Orthogonal): "The current market is obsessed with 'Efficiency' (Competitor A, B, C). We believe the real problem is 'Latency.' While they optimize for cost, we are the only infrastructure built for real-time execution. We are not competing on price; we are selling time."

Result: You have shifted the axis of evaluation. You cannot be compared to Competitor A because you are solving a different variable entirely.

Step 2: The Metric Isolation Framework

Choose a "North Star" metric that your competitors cannot optimize for because their business model prevents it.

The Equation:

Differentiation = (Your Uniquem Metric) / (Industry Standard Metric)

Example: If everyone in the batch is reporting "User Growth" (a commodity metric), you report "Network Density" or "Revenue per Node."

If you are a vertical SaaS:

Don't report: "100 Customers."

Report: "85% Market Share of the Tri-State Area."

Why? It proves dominance, not just participation.

Step 3: The "Binary Choice" Narrative

Frame the investment decision not as "Us vs. Them," but as "The Old World vs. The New World."

Old World: Manual workflows, disparate tools, high error rates (The status quo + your competitors).

New World: Autonomous execution, unified data layer, zero-error guarantee (You).

Force the investor to choose a philosophy, not a vendor. If they buy the philosophy, you are the only logical provider.

The "Death Traps": How Founders Self-Sabotage the Fix

Attempting to differentiate often leads to "Over-Correction," which is equally fatal. Avoid these specific traps:

1. The "No Competitors" Delusion

Never, under any circumstances, include a slide that says "We have no competitors."

The VC View: This translates to "I have done zero research" or "There is no market for this."

The Fix: Always acknowledge the status quo (Excel, Pen & Paper) and the incumbents. Show why you are structurally different, not that you exist in a vacuum.

2. The "Feature Salad" Differentiator

Do not try to win by having more features.

The Trap: A comparison table with 20 rows of checkmarks where you have all green checks and competitors have red X's.

The Reality: VCs know you are cherry-picking. No one believes you are better at everything.

The Fix: Focus on the One Critical Wedge where you win decisively. Admit where you are weaker to gain credibility on where you are stronger.

3. The "Buzzword" Shield

Using "AI," "Blockchain," or "Quantum" as your primary differentiator is suicide in 2026. These are technologies, not value propositions. Unless you have a PhD-level breakthrough, these are just implementation details. Focus on the outcome leverage, not the tech stack.

The "High-Ticket" Conclusion

The difference between being "just another deck in the batch" and the "outlier" is roughly $1M - $3M in pre-money valuation. If you are comparable, you get market-average terms (or no terms). If you are incomparable, you dictate the price. You are not begging for capital; you are selling a slot on a rocket ship that is leaving with or without them.

This requires a holistic restructuring of your entire narrative, from the first hook to the final ask. For a comprehensive breakdown of the entire ecosystem, review How VC Pitch Decks Really Work in 2026 — And Why Most Founders Get Them Wrong.

The Filter Plug: You can attempt to guess which metrics will separate you from the herd, or you can simply execute the proven code. This specific differentiation strategy is automated in our $5k Consultant Replacement Kit. specifically within The Slide-By-Slide VC Instruction Guide, which gives you the exact blueprint to de-commoditize your startup slide by slide.

We sell this for $497 to filter out the hobbyists from the founders ready to close.

You can build this manually, or use the Slide-By-Slide VC Instruction Guide included in our $5k Consultant Replacement Kit ($497) available on the home page.

Funding Blueprint

© 2026 Funding Blueprint. All Rights Reserved.