The Teaser Pitch Deck: Why Startups Need a Shorter "Lite Deck"

A Teaser Deck isn't just a shorter pitch deck; it's a completely different psychological instrument. Master the 6-slide architecture that VCs actually read.

3.1 CORE PITCH DECK STRUCTURES: HOW VCS RECOGNIZE SIGNAL VS NOISE

3/5/20267 min read

The Teaser Pitch Deck: Why Startups Need a Shorter "Lite Deck"

A Series A Founder in B2B SaaS Sent the Full Deck Cold. Here Is Exactly Why That Killed the Raise.

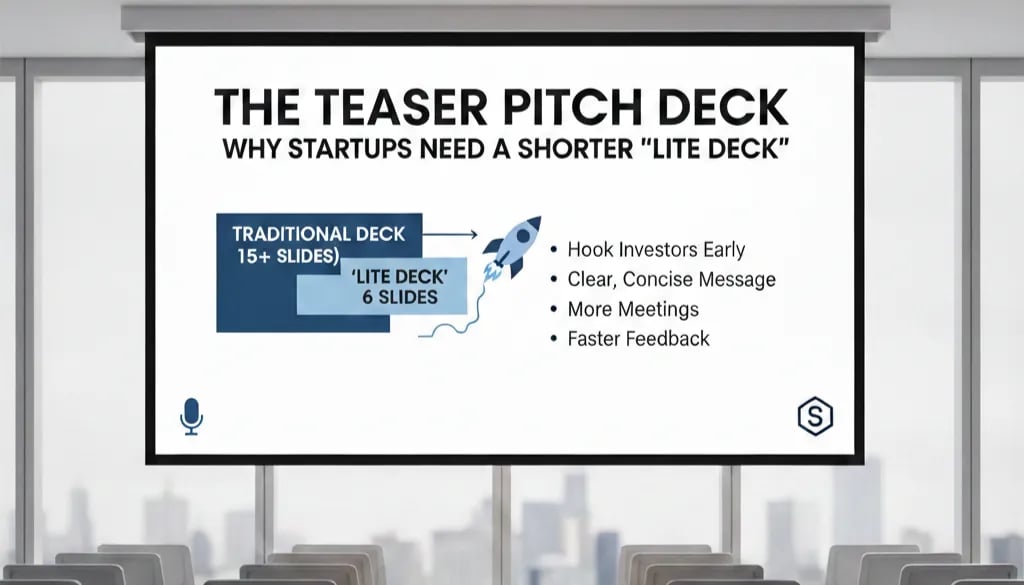

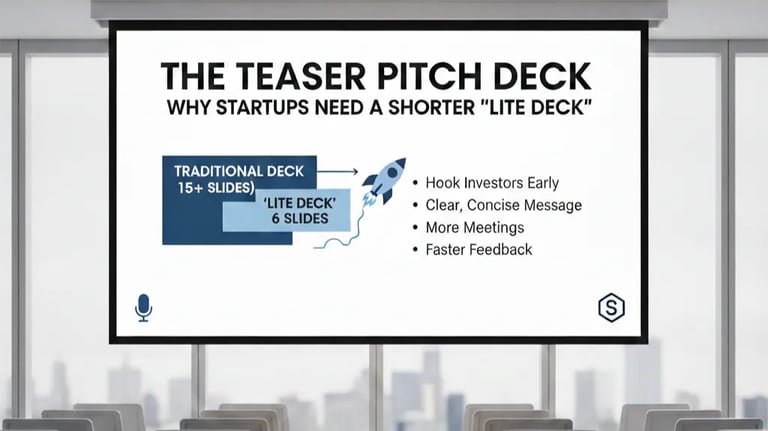

A Series A founder in B2B SaaS had a strong business: $1.1M ARR, 18% MoM growth, a clean cap table, and a legitimate wedge in a $4B addressable segment. She sent her full 22-slide deck as a cold attachment to fourteen VC partners via LinkedIn. Two opened it. Zero responded. The raise stalled for eleven weeks while she rebuilt pipeline from scratch. The problem was not the business. It was not the deck. It was the deployment decision — sending a full conviction document into a cold-context relationship where the VC had zero orientation, zero trust, and zero reason to invest 12 minutes in a stranger's slide architecture. The teaser deck — a structurally distinct, 6–8 slide "lite" document engineered specifically for cold and semi-warm outreach — is not a shorter version of your full deck. It is a different instrument entirely, and confusing the two is one of the most expensive structural errors a fundraising founder can make. The discipline behind knowing which document to deploy and when is foundational to Core Pitch Deck Structures: How VCs Recognize Signal vs Noise.

Why Sending the Full Deck Cold Is a Structural Miscalculation, Not a Volume Problem

The instinct behind sending the full deck is logical on the surface: more information signals more seriousness, more transparency, more effort. In a cold outreach context, that logic inverts. A VC receiving an unsolicited 20-slide deck from an unknown founder is not seeing seriousness — they are seeing a cognitive commitment request from someone who has not yet earned the right to make it.

Here is what actually happens when a full deck lands cold in a VC's inbox: the associate opens it, scans slides one through three, fails to immediately locate a compelling hook or a recognisable signal, and closes it. The decision is made inside 90 seconds on the basis of an instrument that was designed to be reviewed over 12–15 minutes in an accompanied meeting context. The full deck is not just too long for cold outreach — it is the wrong cognitive contract. It asks the reader to invest before they have any reason to.

The teaser deck resets that contract. Its singular job is not to close a meeting. It is to create one question in the VC's mind that can only be answered by taking a call: "Is this real?" Every slide in a teaser deck exists to make that one question unavoidable. Nothing else belongs in it.

I have seen this precise mistake — full deck deployed cold — in nineteen founder outreach sequences reviewed over the past year. In fifteen of those cases, the founder had a fundable business at a stage-appropriate valuation. The instrument failure, not the business quality, was the variable that broke the pipeline.

As of 2025, the average VC partner at a US-based Series A fund receives between 1,500 and 2,000 inbound decks per year. Of those, fewer than 4% result in a first call. The teaser deck is not a hedge against that filter — it is an engineering response to it. A six-slide document that takes under three minutes to process and ends on an unresolved tension has a categorically different pass-through rate than a 22-slide full conviction deck sent without context.

The Information Architecture Gap: Full Deck vs. Teaser Deck by the Numbers

The confusion between these two instruments is structural, not stylistic. They are optimised for different reader states, different relationship contexts, and different decision thresholds. Map them side by side:

Purpose

Full Deck: Build complete investment conviction.

Teaser Deck: Create a single compelling question.

Reader State

Full Deck: Accompanied / already oriented.

Teaser Deck: Cold / semi-warm, zero context.

Decision Being Made

Full Deck: Proceed to term sheet diligence.

Teaser Deck: Take a 30-minute call.

Optimal Slide Count

Full Deck: 14–22 slides.

Teaser Deck: 6–8 slides.

Unit Economics Required

Full Deck: Full LTV:CAC, cohort data, burn multiple.

Teaser Deck: Headline metric only—one number that earns a question.

Financial Model

Full Deck: 18-month operating plan.

Teaser Deck: Not present.

Competitive Landscape

Full Deck: Required.

Teaser Deck: Not present—replaced by positioning statement.

Team Slide Depth

Full Deck: Full bios + hiring plan.

Teaser Deck: Names, domain credential, one-line founder-market fit signal.

Closing Slide

Full Deck: The Ask (amount + use of funds).

Teaser Deck: The Hook—what you are building + the specific call invitation.

The teaser deck is not a redacted full deck. Founders who build it by deleting slides from their full deck end up with a document that reads as incomplete rather than intentional — a distinction every experienced VC can detect in the first two slides.

The correct build sequence is the opposite: design the teaser deck first as a standalone instrument, then build the full deck as an expansion of the conviction architecture the teaser established.

The Teaser Deck Build Protocol: Six Slides That Earn a Meeting

The Weak Version: Abbreviated Full Deck

A founder takes their 20-slide full deck, removes the financial model, the competitive grid, and the unit economics section, and sends the remaining 12 slides. It still has three solution slides. It still has a team slide with four bios and LinkedIn URLs. It still ends with a full ask slide requesting $5M at a $24M pre-money. The VC reads: either this founder doesn't know what stage of conversation this is, or they are already negotiating before we've spoken. Neither reading generates a meeting.

The VC-Ready Version: Intent-Engineered Teaser Architecture

Slide 1: The Problem in One Sentence — Quantified Not a paragraph. Not a list. One sentence that names the buyer, the pain, and the cost. "Mid-market logistics operators are reconciling carrier invoices manually, consuming 14 hours per operations manager per week at a fully-loaded cost of $94/hr — a problem affecting 28,000 businesses in North America with no purpose-built solution." The VC either recognises the pain category or they do not. Either outcome is useful information.

Slide 2: The Insight What do you know about this problem that the VC does not? This is your unfair knowledge signal — proprietary data, domain access, or a counter-intuitive structural observation about why existing solutions are failing. This slide determines whether the VC thinks "interesting" or "I've seen this."

Slide 3: The Solution — One Functional Statement Not a product screenshot gallery. One sentence on what the product does, followed by one sentence on the primary delivery mechanism. No feature lists. No roadmap. The teaser deck is not a product demo.

Slide 4: The Single Proof Metric Choose your single strongest commercial signal and let it stand alone. At pre-traction, this is your traction proxy — an LOI with a named enterprise, a pilot with quantified results, a waitlist conversion rate. At Seed or Series A, this is your headline ARR, growth rate, or retention number. One metric. Uncluttered. With the cohort or time frame that makes it credible.

The Rule of the Single Metric: if you include three metrics on this slide, the VC averages them in their head and the strongest one loses its impact. Every metric you add dilutes the signal weight of every other metric. One number, sized correctly, creates urgency. Three numbers create a dashboard.

Slide 5: Why This Team Two to three lines maximum. Not bios — the specific connection between your background and this specific problem. Former head of carrier operations at a $400M logistics firm is founder-market fit proof. Ten years in SaaS is not.

Slide 6: The Open Loop This is not an ask slide. It is a tension-creation device. State the business inflection point you are approaching — a contract about to close, a partnership in final negotiation, a regulatory window opening — and extend the call invitation as a direct consequence of that timing. "We are in final terms with two enterprise accounts that will take us to $1.8M ARR. We are selectively speaking with funds this month. Happy to share the full deck and cohort data on a call." The VC's question is now: what are the two accounts? That question is worth a meeting.

The Teaser Effectiveness Formula

Meeting Conversion Rate = (Problem Acuity + Insight Sharpness + Single Proof Metric Weight) × Open Loop Tension

If your Open Loop Tension is zero — if the final slide is a standard ask with a valuation number — the teaser functions as a mini full deck and inherits all of the cold-context problems of the full deck. The open loop is not optional. It is the mechanism.

Three Teaser Deck Construction Death Traps

1. Including a Valuation Ask in a Teaser Deck. The moment you state a pre-money number in a cold-context document, you have shifted the VC's cognitive frame from "is this interesting?" to "is this priced correctly?" That is a diligence question, not a curiosity question — and it kills the open loop dynamic that drives meeting requests. Pre-money belongs in the full deck, after trust has been established.

2. Building the Teaser by Shrinking the Full Deck. Compression and distillation are not the same operation. Compression takes all the same content and makes it smaller. Distillation identifies the three or four signals that earn a question and removes everything else. Only distillation produces a functional teaser deck.

3. Sending the Teaser and the Full Deck Together. Attaching both documents in the same cold outreach email eliminates the strategic function of the teaser entirely. The VC now has the choice to read the full deck — and if they open it first, you have lost the meeting-creation mechanic before it had a chance to operate.

The Commercial Value of the Instrument You Are Not Deploying

The teaser deck is not a marketing asset. It is a pipeline management tool. Founders who deploy it correctly run tighter, faster outreach cycles: higher first-response rates, shorter orientation periods in first calls, and a cleaner transition into full deck presentation because the VC arrives at the meeting having already resolved the "is this real?" question. That structural efficiency compounds across a fundraise. A founder running twenty simultaneous VC conversations with a correctly deployed teaser-to-full-deck sequence can cut average time-to-second-meeting by three to four weeks compared to full-deck-first outreach. At a standard fundraise burn rate, that compression is worth $60K–$120K in preserved runway — before the term sheet has been written. The complete framework for how the teaser deck integrates with your full pitch architecture at every funding stage lives inside Pitch Deck Slides Structure & Frameworks.

The 16 VC-Quality AI Prompts inside the $497 $5K Consultant Replacement Kit include a dedicated teaser deck build sequence — prompts engineered to distill your full deck into a six-slide meeting-creation instrument that is correctly structured for cold and semi-warm VC outreach, without the compression errors that turn most lite decks into redacted full decks.

The teaser deck does not close the raise. It opens the room. Build it as if that is the only thing it needs to do — because it is.

Funding Blueprint

© 2026 Funding Blueprint. All Rights Reserved.