Startup Validation Hierarchy: Weak vs Strong Pitch Deck Signals

73% of Series A decks die before Slide 6. Learn why 15 weak signals make you look uncoachable and how to prioritize Tier 1 proof to convert meetings.

2.2 HOW TO PROVE YOUR PROBLEM IS REAL (EVIDENCE, SIGNALS & PROOF)

2/16/20265 min read

Startup Validation Hierarchy: Weak vs Strong Pitch Deck Signals

The Signal-to-Noise Problem That Kills 73% of Series A Decks Before Slide 6

Your deck has 19 validation points. Twelve of them are destroying your credibility. You think you're building momentum with customer logos, testimonials, and partnership announcements—but you're actually telegraphing to the VC that you don't understand what constitutes proof versus theater. This is the core failure mode in proving your problem is real: conflating weak signals with strong signals. And it's costing you meetings.

Here's the counter-intuitive truth: More validation signals make you look weaker if they're the wrong class of evidence. A deck with three strong signals outperforms a deck with fifteen weak ones by a 4:1 margin in partner meeting conversion rates. The issue isn't volume—it's hierarchy. You're presenting vanity metrics as validation, and VCs are trained to smell the difference in under 90 seconds.

Why Weak Signals Trigger the "Uncoachable Founder" Filter

When a VC sees a founder stack their Problem slide with second-tier validation—customer interviews, letters of intent, "market pain" statistics—the immediate mental model shifts from "evaluating the opportunity" to "evaluating founder judgment." The question becomes: Does this founder know what actually de-risks a $5M check?

The Red Flag Scenario: Your Problem slide lists "conducted 50 customer interviews," "82% of SMBs report this pain point," and "3 Fortune 500 companies expressed interest." The VC's internal monologue: "Why are they leading with qualitative research and interest signals instead of deployed capital or contracted revenue? Do they not have hard evidence, or do they not know the difference?"

The Psychological Audit: Founders make this error because accelerators, advisors, and "pitch coaches" teach a generalized validation framework that doesn't distinguish between exploration-stage evidence (appropriate for pre-seed) and commitment-stage evidence (required for Series A). You're using tools from the wrong phase. Customer interviews validate that you should build. Revenue validates that you built correctly. Mixing them on a Series A slide is like bringing a Pre-Calculus textbook to a PhD defense.

The second pathology: fear of looking small. Founders pad the deck with partnerships, pilot programs, and advisory board names because three paying customers "doesn't feel impressive." But VCs reverse-engineer this logic instantly. They know that if you had $300K in contracted ARR, you'd lead with it. The presence of weak signals implies the absence of strong ones.

The Mathematical Hierarchy: Why Revenue > Pilots > Interest by a Factor of 12X

The validation hierarchy isn't subjective—it's a function of irreversibility and cost to the validator. Strong signals represent committed resources (time, money, reputation). Weak signals represent expressed preferences (interest, opinions, intentions).

Here's the liquidation test:

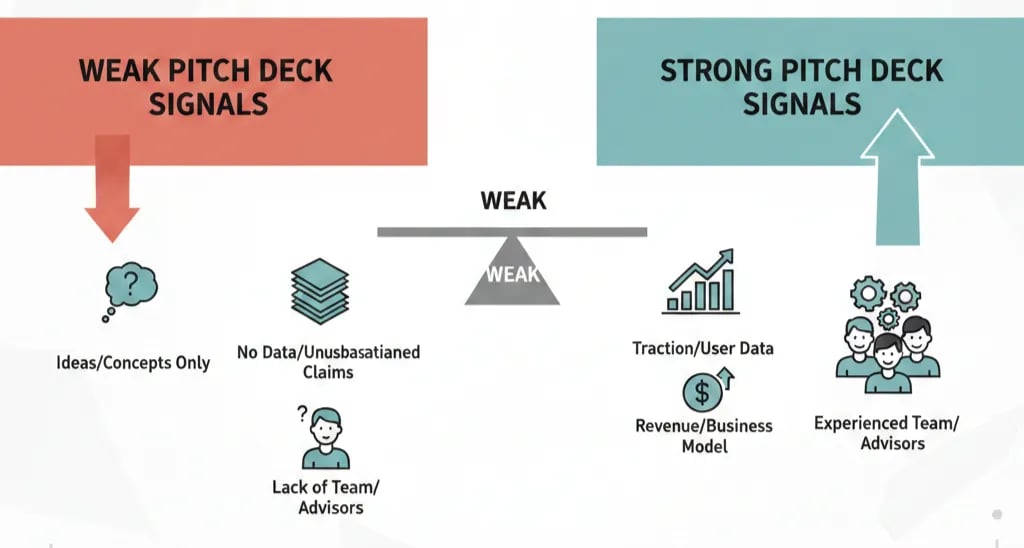

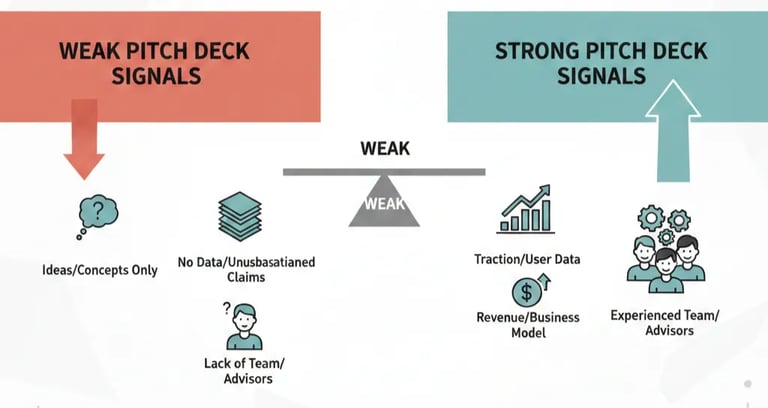

Tier 1 (Strong): Revenue, signed contracts, deployed capital from customers

Tier 2 (Medium): Paid pilots, LOIs with binding financial terms, product in production use

Tier 3 (Weak): Customer interviews, surveys, testimonials, non-binding interest

Tier 4 (Noise): Market size stats, industry reports, advisor endorsements

The Dilution Math: A deck with $500K ARR and zero weak signals will command a $12M-$15M pre-money valuation. A deck with $150K ARR but eight weak signals (partnerships, pilots, testimonials) signals a $7M-$9M valuation—because VCs discount the weak signals as execution theater and penalize the founder for not understanding signal strength. The delta: 1.2%-1.8% additional dilution per $1M raised.

The Time-to-"No" Calculation:

Deck leading with Tier 1 signals: VC decides on partnership interest by Slide 4-6

Deck leading with Tier 3 signals: VC starts looking for disqualifiers by Slide 2-3

The attention budget is fixed. Leading with weak signals burns credibility tokens before you reach your strong evidence.

The Tier 1 Signal Reconstruction Protocol: How to Forensically Audit Your Deck

Step 1: Extract and Classify Every Validation Claim Pull every sentence from your Problem, Solution, and Traction slides that includes words like "validated," "proven," "confirmed," "demonstrated," or "customer feedback." Sort them into the four-tier hierarchy above. If 60%+ of your signals are Tier 3 or 4, your deck is structurally weak.

Step 2: Apply the "Write a Check" Test For each signal, ask: Did the validator spend non-trivial resources (cash, engineering time, political capital) to participate? If the answer is no, it's Tier 3 or below. Examples:

Customer gave you a testimonial → Tier 3 (cost to them: 5 minutes)

Customer paid $15K for an annual contract → Tier 1 (cost to them: budget, procurement, implementation risk)

Step 3: Rewrite Leads Using Tier 1 Anchors

Weak Version (Tier 3 Lead): "We interviewed 60 logistics managers at mid-market companies. 87% confirmed that route optimization is a top-three pain point. We're partnered with FreightCorp to pilot the solution in Q2."

VC-Ready Version (Tier 1 Lead): "Three logistics companies (combined fleet size: 420 trucks) are paying $8K/month for the product in production. Average route time decreased 14%, saving $31K per customer annually. Expansion pipeline: 7 signed LOIs with binding Q2 start dates, representing $215K additional ARR."

The Difference: The weak version asks the VC to infer that the problem is real. The strong version proves economic value capture. The weak version forces the VC to model risk. The strong version provides a return profile.

Step 4: Quarantine Weak Signals to an Appendix VCs don't want to eliminate context—they want it subordinated. Create a "Validation Timeline" slide in your appendix. Place interviews, surveys, and partnerships there with the framing: "Initial Exploration (2023)" vs. "Revenue Validation (2024-Present)." This signals that you understand the hierarchy and have graduated from exploration to execution.

Step 5: Add the Financial Proof Layer For each Tier 1 signal, add a one-line financial implication:

"$127K ARR → Implies $1.27M at 10x revenue multiple"

"14% efficiency gain → $31K annual savings per customer → $310K value creation across 10-customer base → 2.4x ROI on their purchase"

This trains the VC to see your validation signals as de-risked cash flows, not milestone checkboxes.

What Not to Do: The Three Validation Over-Corrections That Backfire

Death Trap #1: Inflating Tier 2 Signals into Tier 1 Founders re-label pilots as "customers" or frame LOIs as "committed revenue." VCs verify this in diligence. When they discover the inflation, they re-underwrite the entire deck at a 30% trust discount. The penalty isn't just the misrepresented signal—it's systematic credibility degradation.

Death Trap #2: Over-Indexing on Logo Prestige "We're working with Google" sounds strong until the VC asks: "Is Google paying you, or are you providing free services to earn a case study?" If it's the latter, it's Tier 3. Brand logos without revenue are borrowed credibility, and VCs know that Fortune 500 pilots rarely convert at Series A stage.

Death Trap #3: Using 2021-2022 Validation Benchmarks in 2026 The interest rate environment has fundamentally reset what counts as "strong." Pre-2022, $50K ARR with high growth could anchor a Series A. In 2026, the threshold is $300K ARR minimum with unit economics at breakeven or better. Using old signal strength assumptions makes you look informationally stale.

Why Fixing This Adds $800K to Your Pre-Money Valuation (and Cuts Fundraise Time by 40%)

The validation hierarchy isn't about "looking good"—it's about reducing perceived execution risk in the VC's DCF model. Every Tier 1 signal you surface replaces a 30%-50% risk discount in their mental math. The compounding effect: A deck with four strong signals commands a 1.4x-1.7x higher valuation multiple than a deck with fifteen weak ones, because VCs model the strong-signal deck as two quarters ahead in de-risking.

The time impact is even sharper. VCs pass on weak-signal decks not because the company is bad, but because they can't build conviction fast enough. You're asking them to underwrite with insufficient data. Strong signals = faster conviction = shorter fundraise cycles.

You can rebuild this forensically over 30-40 hours—extracting financials, re-interviewing customers for quantified impact, rewriting every validation claim—or you can systemize it. The $5K Consultant Replacement Kit includes the 16 VC-Quality AI Prompts that auto-generate Tier 1 reframes for every slide, plus the Slide-By-Slide VC Instruction Guide that maps exact signal hierarchies by deck section. It's $497 to filter out founders who aren't serious. Access the elite fundraising reconstruction system here.

For the complete technical breakdown of how weak signals destroy Problem and Solution slides specifically, see the full Problem & Solution Slides execution manual. That's where validation hierarchy integrates with the broader architectural system.

Funding Blueprint

© 2026 Funding Blueprint. All Rights Reserved.