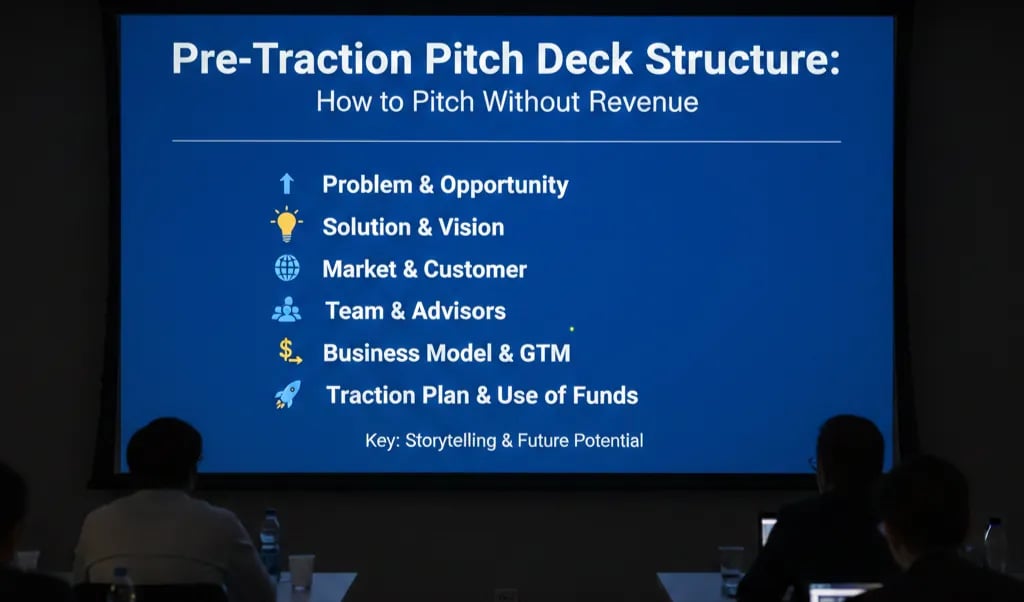

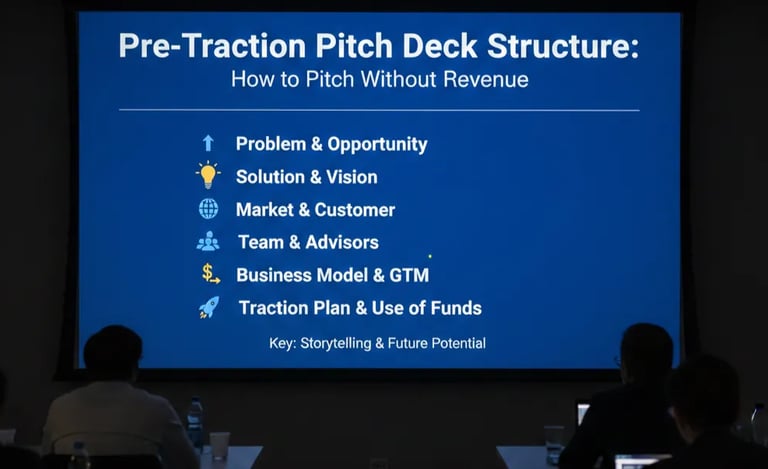

Pre-Traction Pitch Deck Structure: How to Pitch Without Revenue

Pitching without revenue? Stop using fake 5-year financial projections. Learn the Signal-First Pitch Deck structure to secure your pre-seed funding.

3.1 CORE PITCH DECK STRUCTURES: HOW VCS RECOGNIZE SIGNAL VS NOISE

3/5/20266 min read

Pre-Traction Pitch Deck Structure: How to Pitch Without Revenue

Most Founders Think No Revenue Is the Problem. They Are Wrong.

Most founders think that lacking revenue is the disqualifying factor in a pre-traction raise. It is not. The disqualifying factor is building a deck structured around evidence you do not have — projection-heavy slides loaded with "anticipated ARR," "expected CAC," and "forecasted churn" that signal one thing to every VC parsing the deck: this founder does not understand what stage they are at. That miscalibration is structural, not circumstantial, and it is detectable within the first three slides. Understanding how to strip that structure out and replace it with what VCs actually want at this stage is the core subject of Core Pitch Deck Structures: How VCs Recognize Signal vs Noise. Pre-traction founders who fix the architecture first raise faster than those who wait for revenue to do the talking.

Why a Revenue-Framed Deck Kills Pre-Traction Raises Before Slide Four

The specific error is substitution. A founder without revenue has no business metrics, so they substitute financial projections. The deck then reads as a forecast document masquerading as a pitch. VCs — particularly at the Series Seed and Pre-Seed level — are not evaluating a business model spreadsheet. They are evaluating founder judgment, market insight, and execution probability. A deck full of five-year revenue curves tells them nothing about any of those three things.

Here is what the bad version looks like in practice: a Financial Projections slide in deck position 5, showing $0 today, $400K ARR by month 18, and $2.8M by year three — with no customer discovery data, no letter of intent, and no cohort logic underpinning the curve. The VC's internal reaction is not skepticism about the numbers. It is a signal read: this founder does not know what to lead with. That is a judgment call about you, not your model.

I have reviewed eleven pre-traction decks in the past two quarters that used this projection-forward structure. Nine of them did not progress past the first associate screen. The psychological root of the mistake is misidentified credibility. Founders assume that showing financial ambition signals commercial seriousness. In a traction-stage deck, it does. At pre-traction, it reads as a substitute for real evidence — and every experienced VC knows the difference on sight.

The deeper driver is usually bad advice. A founder reads a Series A teardown, copies the financial architecture, and strips out the revenue line because they don't have one yet. What remains is a skeleton that was designed to carry weight it is no longer carrying.

The Mathematical Case for a Signal-First Structure

At the pre-traction stage, VCs are not underwriting a financial model. They are pricing a probability bet. The question they are actually asking is: what is the likelihood this team identifies a real problem, builds a product people pay for, and generates enough early signal to justify a Series A in 24–36 months?

That is not a DCF question. It is a signal question. Your deck architecture must answer it in this order:

Problem Acuity — Is the pain specific, frequent, and expensive? (Not: "SMBs struggle with invoicing." Yes: "Finance teams at 20–200 person B2B SaaS companies reconcile vendor invoices manually, averaging 11 hours per week per analyst at a fully-loaded cost of $68/hr.")

Insight Sharpness — What do you know about this problem that the market does not? This is your unfair insight, not a market size number.

Founder-Market Fit Proof — Why are you the person who finds this? Previous domain experience, proprietary access, or asymmetric knowledge.

Traction Proxy — If you have no revenue, what is the closest thing to it? LOIs, design partners, waitlist conversion rates, pilot commitments, usage data from a prototype.

As of early 2026, top-tier US seed funds — including those running $50M–$150M vintage vehicles — are explicitly benchmarking pre-traction raises against the quality of the "traction proxy," not the absence of revenue itself. A signed LOI from a recognizable enterprise name at pre-seed carries more weight in a partner meeting than a financial model showing $5M ARR at month 30.

The math is simple: a weak traction proxy + strong founder-market fit = fundable. A strong projection model + weak problem framing = not fundable, regardless of the numbers on the page.

The Pre-Traction Deck Protocol: Structure That VCs Will Not Skip

Weak Version vs. VC-Ready Version

Weak Version (Revenue-Framed Pre-Traction Deck):

Slide 1: Title / Tagline

Slide 2: Market Size (TAM/SAM/SOM pyramid)

Slide 3: The Problem (2 bullet points)

Slide 4: The Solution (product screenshot)

Slide 5: Financial Projections ($0 → $2.8M)

Slide 6: Team

Slide 7: Ask

This deck has a logical sequence borrowed from post-traction pitches. At pre-traction, it is structurally dishonest. Every slide after Slide 3 is floating without an evidence base.

VC-Ready Version (Signal-First Pre-Traction Deck):

Slide 1: The Specific Problem (one sentence, quantified)

Slide 2: The Insight (what you know that others don't)

Slide 3: Why Now (market timing catalyst — regulatory shift, infrastructure change, behavioral shift)

Slide 4: The Solution (minimum viable framing — what it does, not what it will eventually do)

Slide 5: Traction Proxy (LOIs, design partners, pilot data, or prototype engagement metrics)

Slide 6: Founder-Market Fit (why this team, why now, why unfair advantage)

Slide 7: Business Model (simple — how does money move, not how much)

Slide 8: The Ask (amount, use of funds, 18-month milestone map)

The Pre-Traction Credibility Equation

Use this as a structural test before you submit a deck:

Pre-Traction Credibility = (Problem Acuity × Founder-Market Fit) + Traction Proxy Weight

If your Problem Acuity score is low (generic pain statement, no quantification), no traction proxy rescues it. If your Founder-Market Fit is weak (no domain connection, no proprietary access), the VC cannot price the probability bet. Both inputs must be strong. Projections are not a variable in this equation.

On the "Why Now" slide: this is the most underbuilt slide in pre-traction decks and the one that most directly signals whether a founder has done real market thinking. A specific market catalyst — not "the market is growing" but "DORA compliance requirements in the UK took effect in January 2025 and have forced mid-market financial institutions to rebuild vendor risk tooling from scratch" — is the difference between a slide a VC skips and a slide a VC photographs with their phone.

Three Pre-Traction Structural Death Traps

1. Adding a Revenue Slide "Just to Show Ambition." It does not show ambition. It shows you do not understand what the investor is pricing at this stage. Remove it.

2. Using TAM as a Credibility Signal. A $40B TAM number on slide two tells a VC nothing about whether your specific wedge is real. Replace the pyramid with a bottoms-up market sizing of your beachhead — the 500 companies, 3,000 users, or specific geography you will own first.

3. Listing Founding Team Credentials Without Connecting Them to the Problem. "10 years at McKinsey" is not founder-market fit. The connection between your background and why you are uniquely positioned to solve this specific problem must be explicit. If you do not make that argument, the VC will assume the answer is "you are not."

What Fixing This Deck Architecture Is Actually Worth at the Table

Structural clarity in a pre-traction deck does not just improve your acceptance rate on first meetings. It compresses the diligence cycle. When a VC can immediately locate the problem, the insight, the proof, and the founder logic, the first meeting moves faster, the follow-up questions are sharper, and the path to a term sheet shortens. In practical terms: founders who present with a clean signal-first structure are more likely to receive a second meeting within two weeks versus four to six weeks for decks that require interpretive work from the VC's side. That timeline compression is not aesthetic — it is a valuation and dilution outcome. A faster close at the same pre-money means less cash burned between first meeting and wire. That gap, across a 12-week fundraise versus a 6-week fundraise, can represent $80K–$150K in runway consumed. Fix the structure, and you are not just improving your pitch. You are improving your cap table. For the full system behind how every slide in your deck interacts with VC pattern recognition, Pitch Deck Slides Structure & Frameworks is the complete architecture.

Every week your pre-traction deck runs with the wrong structure is a meeting you will not get back. The Slide-By-Slide VC Instruction Guide inside the $497 $5K Consultant Replacement Kit is built specifically for pre-traction founders — it maps exactly which signals belong on which slide and in what order, so you walk into your first VC meeting with a deck that already answers the questions their analyst will ask before you enter the room.

The pre-traction raise is won or lost on structural judgment, not financial projection. Build accordingly.

Funding Blueprint

© 2026 Funding Blueprint. All Rights Reserved.