The Modern 12-Slide Pitch Deck Format Used by Funded Startups

VCs read pitch decks in 2 minutes and 42 seconds. Learn the exact 12-slide sequence funded startups use to survive the Series A analyst screen.

3.1 CORE PITCH DECK STRUCTURES: HOW VCS RECOGNIZE SIGNAL VS NOISE

3/4/20266 min read

The 12-Slide Pitch Deck Format Funded Startups Actually Use (And Why Yours Is Probably Wrong)

Most founders think adding more slides makes their pitch more compelling. It makes it a liability.

The modern Series A pitch deck is not a document. It is a filtering mechanism — and the filter runs in both directions. A VC's analyst screens your deck before a partner ever sees it, and the structure of those 12 slides determines whether you get escalated or archived. If you are building a deck without understanding the forensic logic behind each slide's position, you are not pitching. You are guessing. This is part of the foundational framework covered in Core Pitch Deck Structures: How VCs Recognise Signal vs Noise — and the sequencing logic below is where most founders bleed out before they realise it.

Why Slide Order Destroys Series A Pitches Before the Financials Are Ever Opened

The most common structural error is not a bad slide. It is a correct slide placed in the wrong position.

Founders default to a logic that feels intuitive: problem, then solution, then market, then traction, then team. That is a natural story arc. It is also the wrong one for a capital allocation decision. VCs are not reading your deck to understand your product. They are running a parallel mental model — asking themselves, at every slide, whether the risk-reward profile of this company justifies the cost of further diligence.

When the Market slide comes before Traction, you are asking the investor to accept your TAM framing before they have any evidence you can execute inside it. That is a trust problem, not a narrative one. When the Team slide is buried at slide 10, you have already asked the reader to evaluate your business without knowing whether to believe the person presenting it.

I have reviewed fourteen Series A decks in the last two quarters where the founder placed the Business Model slide after the Financials — in every case, the VC's first question in follow-up was "I still don't understand how you make money." That question should not exist by slide 9. The mistake is not ignorance of the content; it is a misunderstanding of what each slide is doing to the reader's decision-making process at the moment they see it.

The psychological driver behind this error is almost always the same: founders structure their deck the way they learned their own business — chronologically, by what they figured out first. That is not how a capital-allocation decision is processed.

The Mathematical Cost of a Missequenced 12-Slide Deck

The average VC spends 2 minutes and 42 seconds on a cold deck. That is not a metaphor — it is a documented behavioural average from Docsend's longitudinal tracking data. Twelve slides at that pace gives you roughly 13 seconds per slide. Cognitive load is not distributed evenly across those 13 seconds.

Here is what the sequencing math actually looks like for a $3M Series A ask:

Slide Position vs. Decision Weight (Analyst Screen)

Slides 1-2 (35% Weight): Focuses on problem comprehension and founder intuition.

Question: "Do I understand the problem and does this founder get it?"

Slides 3-5 (30% Weight): Focuses on market validation and demand.

Question: "Is the market real and is there evidence of pull?"

Slides 6-8 (20% Weight): Focuses on monetization and unit economics.

Question: "Does the model make money and is the unit economics story coherent?"

Slides 9-10 (10% Weight): Focuses on team capability.

Question: "Can this team execute this?"

Slides 11-12 (5% Weight): Focuses on the "Ask" and capital allocation.

Question: "What are they asking for and what is the use of funds?"

The implication is brutal: if your Traction slide is at position 9, it receives 10% of the attention it would have commanded at position 4. At position 4, traction reframes everything that follows. At position 9, it is a footnote.

As of early 2026, top-tier US funds are applying a stricter pre-screen protocol — partner time is down, analyst gates are up, and the median time between first deck submission and first partner meeting has extended to 18–22 business days at Tier 1 funds. A missequenced deck does not get a second look. It gets a template rejection and a 90-day cooldown before re-engagement is considered.

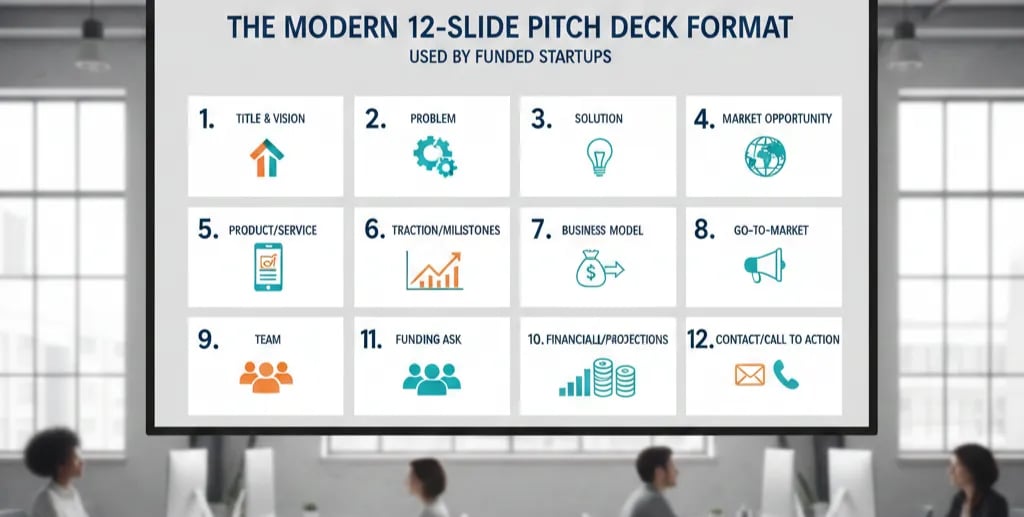

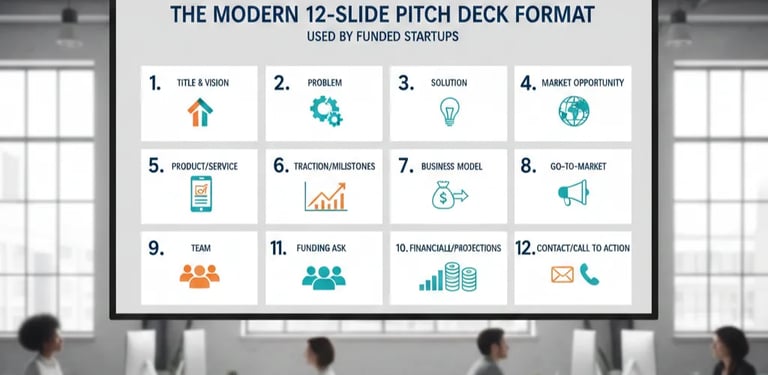

The VC-Ready 12-Slide Architecture: Sequence, Function, and Signal

This is not a list of slide names. It is a decision-forcing sequence.

The Correct Structure:

Cover — Company name, one-line positioning statement, contact. No "About Us." No mission statements.

Problem — One specific, expensive problem. Quantified if possible. Not three problems. One.

Solution — What you do, in plain language. No feature lists. No product screenshots yet.

Traction — This is the early credibility anchor. MRR, growth rate, logo count, or a pipeline figure. Place it here, not at slide 9.

Market Size — TAM/SAM/SOM, but built bottom-up. A top-down TAM figure from a Gartner report is not a market size. It is a citation dressed as analysis.

Product — Screenshots, demo flow, or architecture. Placed after the reader has decided the problem is real and the company has evidence of demand.

Business Model — How you charge, what the unit looks like, and what happens to margin at scale.

Go-To-Market — Acquisition channels with CAC data if available. Not a list of marketing tactics.

Competition — A 2×2 matrix is acceptable only if the axes are non-obvious. Axes of "price vs. features" belong in 2018.

Team — Key founders, relevant domain experience, and one credibility signal per person (exits, domain tenure, customer relationships).

Financials — Three-year projection with assumptions visible. Burn rate, runway, and the month you hit break-even or next milestone.

The Ask — Amount, instrument (SAFE, priced round, convertible), use of funds in three line items maximum.

Weak Version vs. VC-Ready Version — The Traction Slide

Weak: "We have 12 customers and are growing." Placed at slide 9.

VC-Ready: "$47K MRR. 34% MoM growth over the last quarter. NRR at 118%. Three design partners signed LOIs for annual contracts." Placed at slide 4, directly after the Solution slide, before the market size is introduced.

The difference is not the data. It is the position of the data in the sequence of belief-building.

The Rule of Irreversible Conviction: By slide 5, a VC should already believe the problem is real, the company has evidence of demand, and the market is large enough to justify the check. If any of those three beliefs is not established by slide 5, the remaining seven slides are fighting an uphill battle against a reader who has already begun composing a polite pass.

Three Structural Death Traps Inside the 12-Slide Format

1. The Solution-First Error. Placing the Solution at slide 2 before the Problem is established. You are asking the reader to evaluate an answer before they accept the question. The VC does not know yet whether to care.

2. The Bloated Market Slide. Including TAM/SAM/SOM on three separate slides, or building a market narrative that runs to 400 words. Market size is a single-slide assertion backed by one bottom-up calculation. It is not a research paper.

3. Using 2021 Comp Multiples on a 2026 Revenue Projection. If your financial model implies a 15× ARR exit multiple for a SaaS business in 2026, post-correction multiples will immediately discredit your model. Post-2024, top-tier SaaS exits are clearing at 6×–9× ARR for companies with strong NRR. Your projection must be internally consistent with the market your VC is deploying into today.

What Restructuring This Deck Is Actually Worth at the Term Sheet Stage

A missequenced 12-slide deck does not just cost you a meeting. It costs you the valuation conversation. Founders who fix their sequencing and compress their narrative into a decision-forcing flow report significantly shorter diligence cycles — because the VC has fewer open questions by the time they reach the financials. Fewer open questions means less negotiating surface. Less negotiating surface means a cleaner term sheet.

The complete system for building a deck that passes analyst screens and survives partner scrutiny is inside the Pitch Deck Slides Structure & Frameworks resource — treat it as the engineering spec, not the inspiration board.

Every week your deck runs in the wrong sequence is a week you are sending a structurally compromised document into a process designed to find reasons to pass. The Slide-By-Slide VC Instruction Guide inside the $5K Consultant Replacement Kit is built specifically to close this gap — it maps the exact logic each slide must satisfy before the next one is earned, so you walk into your next partner meeting with a deck already calibrated against what the analyst will check. The full Kit is $497. Access it at the Slide-By-Slide VC Instruction Guide inside the $5K Consultant Replacement Kit.

The deck is not the pitch. The sequence is the pitch. Fix the sequence first.

Funding Blueprint

© 2026 Funding Blueprint. All Rights Reserved.